Suspense Accounts and Control Accounts

VerifiedAdded on 2021/02/22

|19

|4976

|94

AI Summary

This assignment delves into the world of accounting, focusing on suspense accounts and control accounts. A suspense account is used to record transactions that have not been ascertained at the time of entry, providing a check on business transactions. Control accounts are utilized to verify balances in subsidiary accounts, ensuring accuracy in financial statements. The assignment also touches upon bank reconciliation, an essential process for identifying discrepancies between bank statements and company records.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Unit 10 - Financial Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

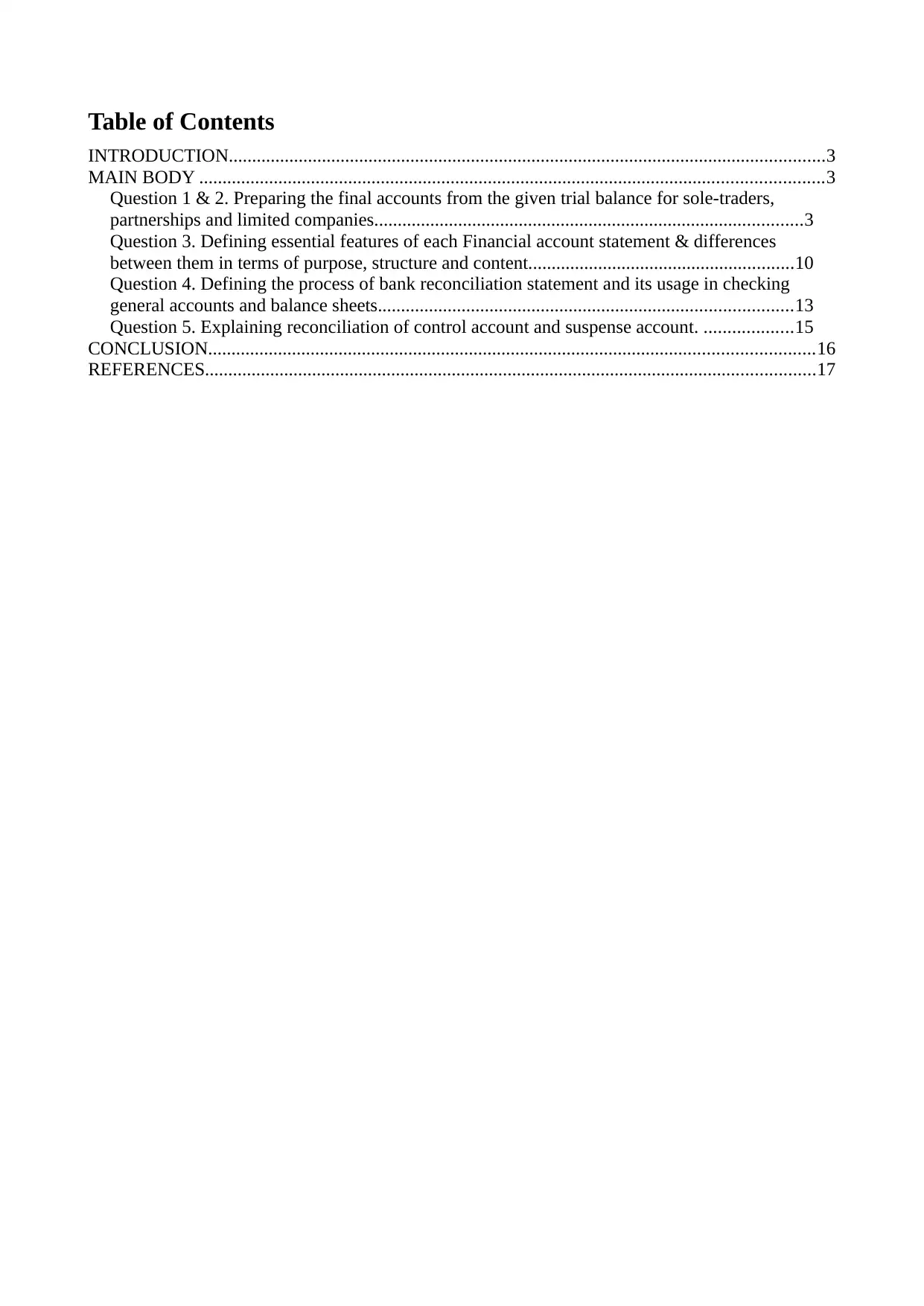

Table of Contents

INTRODUCTION................................................................................................................................3

MAIN BODY ......................................................................................................................................3

Question 1 & 2. Preparing the final accounts from the given trial balance for sole-traders,

partnerships and limited companies............................................................................................3

Question 3. Defining essential features of each Financial account statement & differences

between them in terms of purpose, structure and content.........................................................10

Question 4. Defining the process of bank reconciliation statement and its usage in checking

general accounts and balance sheets.........................................................................................13

Question 5. Explaining reconciliation of control account and suspense account. ...................15

CONCLUSION..................................................................................................................................16

REFERENCES...................................................................................................................................17

INTRODUCTION................................................................................................................................3

MAIN BODY ......................................................................................................................................3

Question 1 & 2. Preparing the final accounts from the given trial balance for sole-traders,

partnerships and limited companies............................................................................................3

Question 3. Defining essential features of each Financial account statement & differences

between them in terms of purpose, structure and content.........................................................10

Question 4. Defining the process of bank reconciliation statement and its usage in checking

general accounts and balance sheets.........................................................................................13

Question 5. Explaining reconciliation of control account and suspense account. ...................15

CONCLUSION..................................................................................................................................16

REFERENCES...................................................................................................................................17

INTRODUCTION

The term financial accounting is defined as a process of monitoring and tracking financial as well as

accounting transactions of the business for a specific time period. It is very much essential for every

business organization to follow proper and accurate financial guidelines, principles and standards at

the time of preparation of final accounts of the company. Financial accounting will help

stakeholders and shareholders in having full knowledge of business transactions as taking place in

the company during an accounting year which indirectly helps them in their decision making

process. By following proper guidelines and norms related to accounting and financial transactions

during recording, summarizing and presenting in financial statements, it will provide deep insight

about companies financial performance. The present will define manner in which final accounts for

sole trader, limited and partnership business is prepared with the help of Trial balance in accordance

with appropriate principles, conventions and standards. Also, report will contain bank reconciliation

process to ensure company and bank records are correct. Further, process related to the preparation

of bank reconciliation will be defined. Also, explanation will be made in context of process taken to

reconcile control accounts and clear suspense accounts.

MAIN BODY

Question 1 & 2. Preparing the final accounts from the given trial balance for sole-traders,

partnerships and limited companies.

Final accounts of the company is also known as the Financial statement which is prepared

for an accounting year as per the accounting standards and norms. It depicts the overview of

company's financial position along with financial transactions taken place in the business for a

specific time period. It should contain all the material disclosure which can have influencing impact

on the decision making process of its investors and other stakeholders. Financial accounts basically

includes an Income statement, Balance sheet etc.

1. Sole traders – Is a type of business organisation which is owned and formed by a single person

who runs its business operations as per own beliefs and decision. All the revenue made and loss

incur are kept and bear by the owner himself. Owner is only personally liable for business liabilities

as due on part of business firm.

Final account of Sole trader

Income statement for the year ended 31st April 2019 of Greg Palmer

Dr Cr

Particulars Amount (£) Particulars Amount (£)

The term financial accounting is defined as a process of monitoring and tracking financial as well as

accounting transactions of the business for a specific time period. It is very much essential for every

business organization to follow proper and accurate financial guidelines, principles and standards at

the time of preparation of final accounts of the company. Financial accounting will help

stakeholders and shareholders in having full knowledge of business transactions as taking place in

the company during an accounting year which indirectly helps them in their decision making

process. By following proper guidelines and norms related to accounting and financial transactions

during recording, summarizing and presenting in financial statements, it will provide deep insight

about companies financial performance. The present will define manner in which final accounts for

sole trader, limited and partnership business is prepared with the help of Trial balance in accordance

with appropriate principles, conventions and standards. Also, report will contain bank reconciliation

process to ensure company and bank records are correct. Further, process related to the preparation

of bank reconciliation will be defined. Also, explanation will be made in context of process taken to

reconcile control accounts and clear suspense accounts.

MAIN BODY

Question 1 & 2. Preparing the final accounts from the given trial balance for sole-traders,

partnerships and limited companies.

Final accounts of the company is also known as the Financial statement which is prepared

for an accounting year as per the accounting standards and norms. It depicts the overview of

company's financial position along with financial transactions taken place in the business for a

specific time period. It should contain all the material disclosure which can have influencing impact

on the decision making process of its investors and other stakeholders. Financial accounts basically

includes an Income statement, Balance sheet etc.

1. Sole traders – Is a type of business organisation which is owned and formed by a single person

who runs its business operations as per own beliefs and decision. All the revenue made and loss

incur are kept and bear by the owner himself. Owner is only personally liable for business liabilities

as due on part of business firm.

Final account of Sole trader

Income statement for the year ended 31st April 2019 of Greg Palmer

Dr Cr

Particulars Amount (£) Particulars Amount (£)

Opening inventory 160000 Sales 1400000

Add: Purchases 840000

Less: Sales

returns 0

Less: Purchase

returns 0

Less: Closing

inventory 100000

1400000

Cost of sales 900000

Gross profit 500000

Expenses: Gross profit c/f 500000

Wages and salaries 460000

Heat and light 80000

Sundry expenses 126000

Depreciation 96000

Gas payment 8000

Net loss 270000

Net loss 770000 Net loss 770000

Statement of financial position at the year ended 31st April 2019 of Greg Palmer

Particulars Amount (£) Amount (£)

Non current Assets

Fixtures and fittings 384000 384000

Current Assets

Trade receivables 160000

Inventory 100000

Prepaid expenses 44000 304000

Total Assets 688000

Current liabilities

Bank overdraft 80000 80000

Non current liabilities

Outstanding Wages 20000

Gas payment

outstanding 8000 28000

Capital 960000

Less: Drawing 110000

Less: Net loss 270000 580000

Total Liabilities 688000

1. Depreciation on Amount (£)

Add: Purchases 840000

Less: Sales

returns 0

Less: Purchase

returns 0

Less: Closing

inventory 100000

1400000

Cost of sales 900000

Gross profit 500000

Expenses: Gross profit c/f 500000

Wages and salaries 460000

Heat and light 80000

Sundry expenses 126000

Depreciation 96000

Gas payment 8000

Net loss 270000

Net loss 770000 Net loss 770000

Statement of financial position at the year ended 31st April 2019 of Greg Palmer

Particulars Amount (£) Amount (£)

Non current Assets

Fixtures and fittings 384000 384000

Current Assets

Trade receivables 160000

Inventory 100000

Prepaid expenses 44000 304000

Total Assets 688000

Current liabilities

Bank overdraft 80000 80000

Non current liabilities

Outstanding Wages 20000

Gas payment

outstanding 8000 28000

Capital 960000

Less: Drawing 110000

Less: Net loss 270000 580000

Total Liabilities 688000

1. Depreciation on Amount (£)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

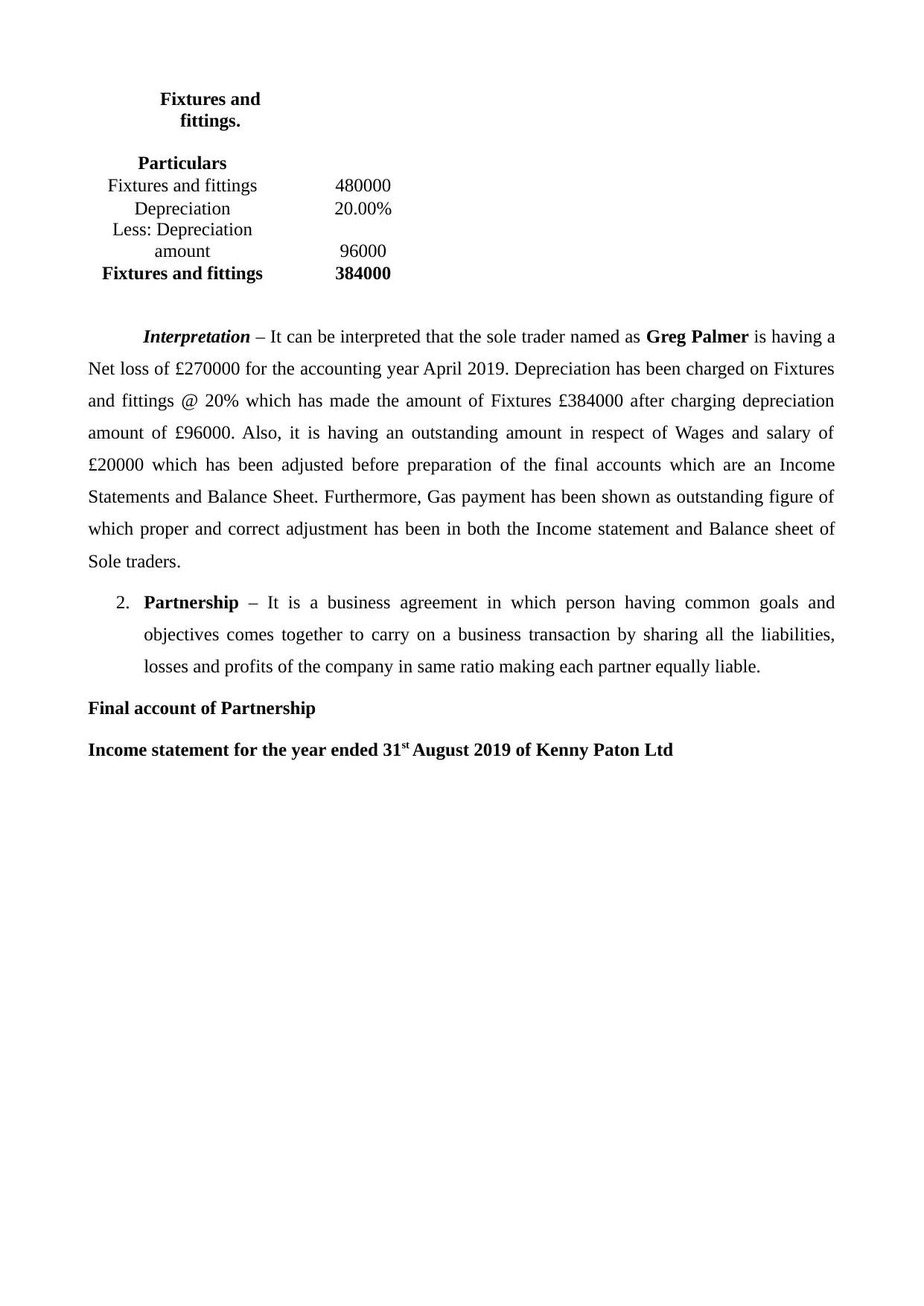

Fixtures and

fittings.

Particulars

Fixtures and fittings 480000

Depreciation 20.00%

Less: Depreciation

amount 96000

Fixtures and fittings 384000

Interpretation – It can be interpreted that the sole trader named as Greg Palmer is having a

Net loss of £270000 for the accounting year April 2019. Depreciation has been charged on Fixtures

and fittings @ 20% which has made the amount of Fixtures £384000 after charging depreciation

amount of £96000. Also, it is having an outstanding amount in respect of Wages and salary of

£20000 which has been adjusted before preparation of the final accounts which are an Income

Statements and Balance Sheet. Furthermore, Gas payment has been shown as outstanding figure of

which proper and correct adjustment has been in both the Income statement and Balance sheet of

Sole traders.

2. Partnership – It is a business agreement in which person having common goals and

objectives comes together to carry on a business transaction by sharing all the liabilities,

losses and profits of the company in same ratio making each partner equally liable.

Final account of Partnership

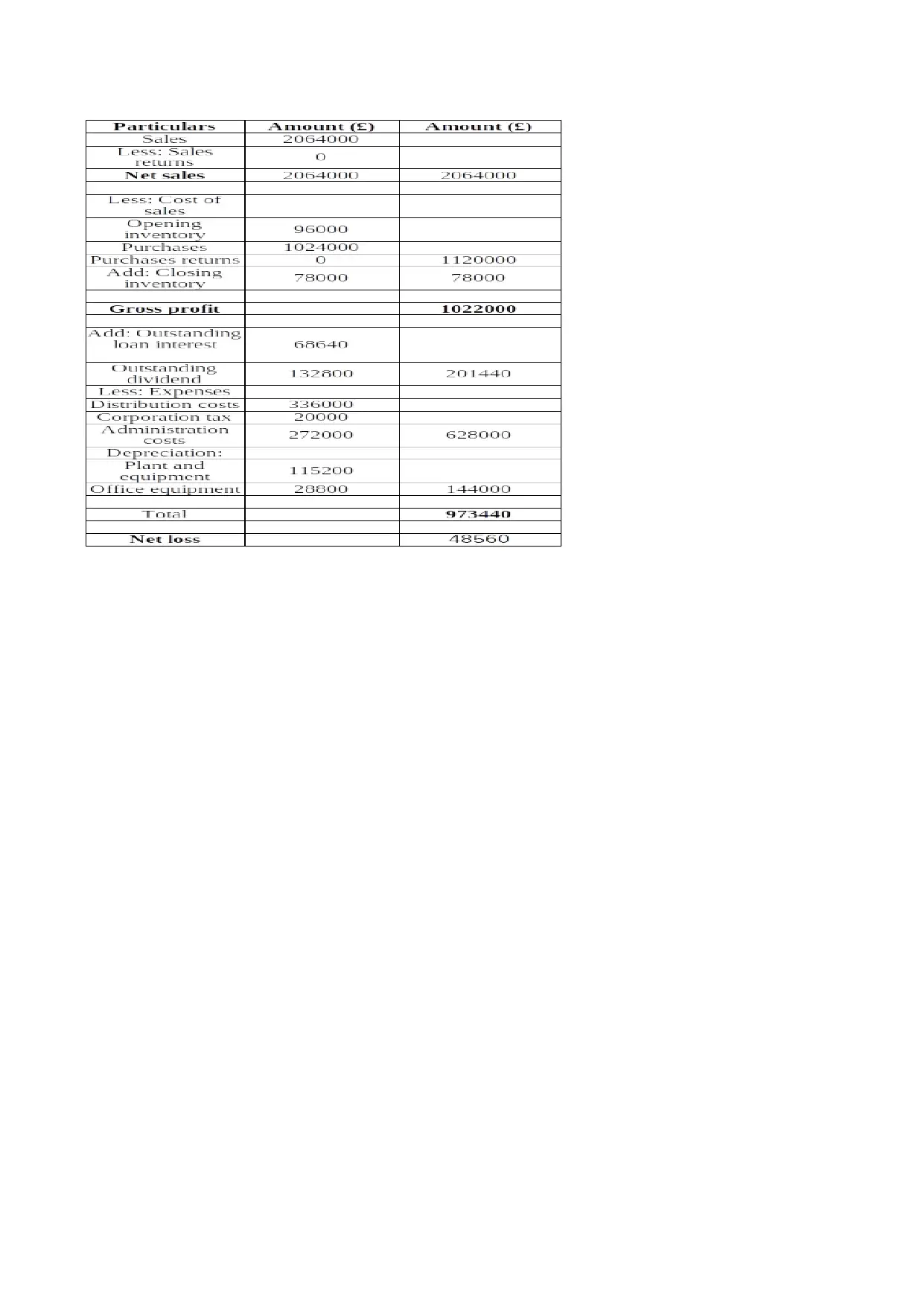

Income statement for the year ended 31st August 2019 of Kenny Paton Ltd

fittings.

Particulars

Fixtures and fittings 480000

Depreciation 20.00%

Less: Depreciation

amount 96000

Fixtures and fittings 384000

Interpretation – It can be interpreted that the sole trader named as Greg Palmer is having a

Net loss of £270000 for the accounting year April 2019. Depreciation has been charged on Fixtures

and fittings @ 20% which has made the amount of Fixtures £384000 after charging depreciation

amount of £96000. Also, it is having an outstanding amount in respect of Wages and salary of

£20000 which has been adjusted before preparation of the final accounts which are an Income

Statements and Balance Sheet. Furthermore, Gas payment has been shown as outstanding figure of

which proper and correct adjustment has been in both the Income statement and Balance sheet of

Sole traders.

2. Partnership – It is a business agreement in which person having common goals and

objectives comes together to carry on a business transaction by sharing all the liabilities,

losses and profits of the company in same ratio making each partner equally liable.

Final account of Partnership

Income statement for the year ended 31st August 2019 of Kenny Paton Ltd

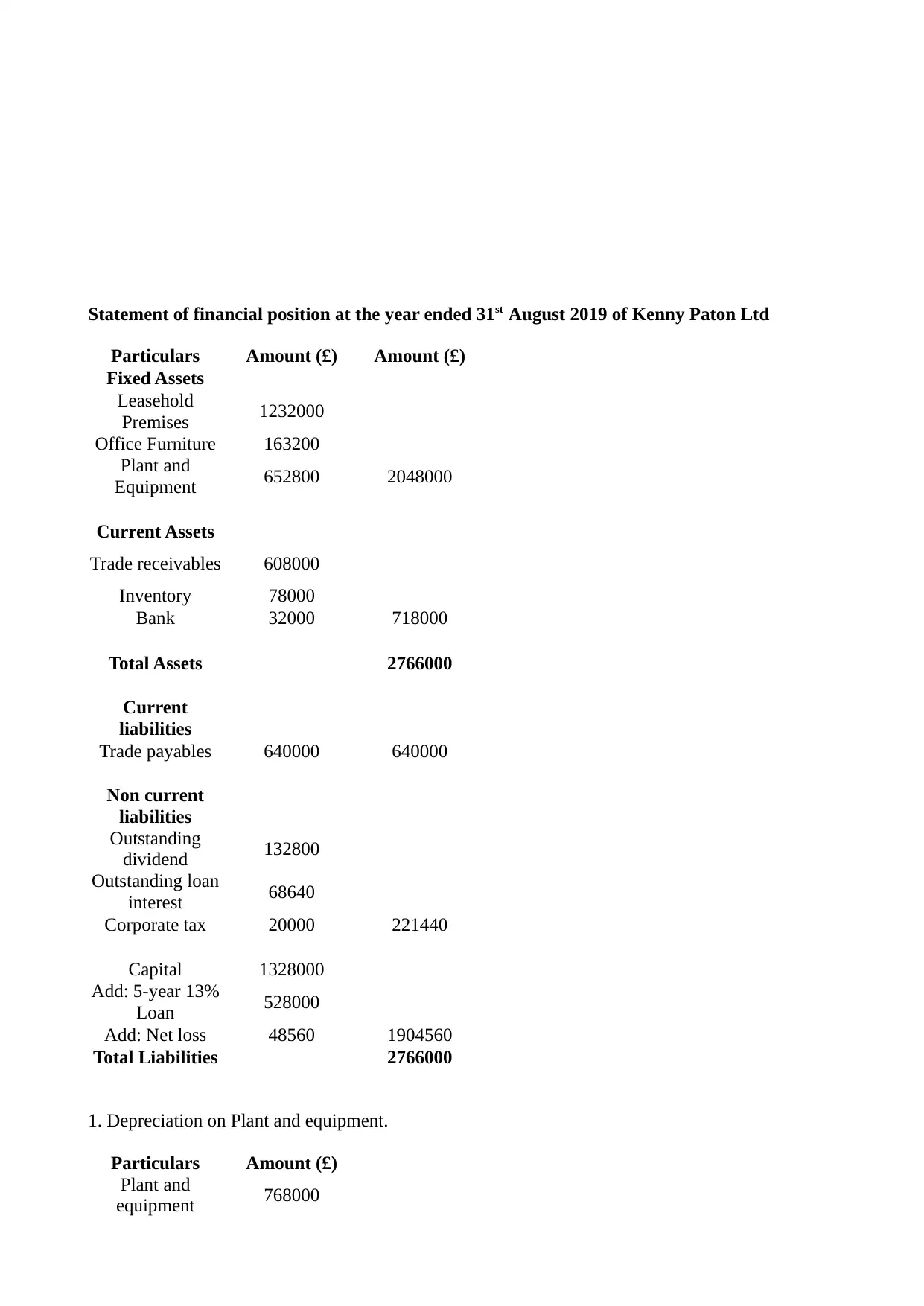

Statement of financial position at the year ended 31st August 2019 of Kenny Paton Ltd

Particulars Amount (£) Amount (£)

Fixed Assets

Leasehold

Premises 1232000

Office Furniture 163200

Plant and

Equipment 652800 2048000

Current Assets

Trade receivables 608000

Inventory 78000

Bank 32000 718000

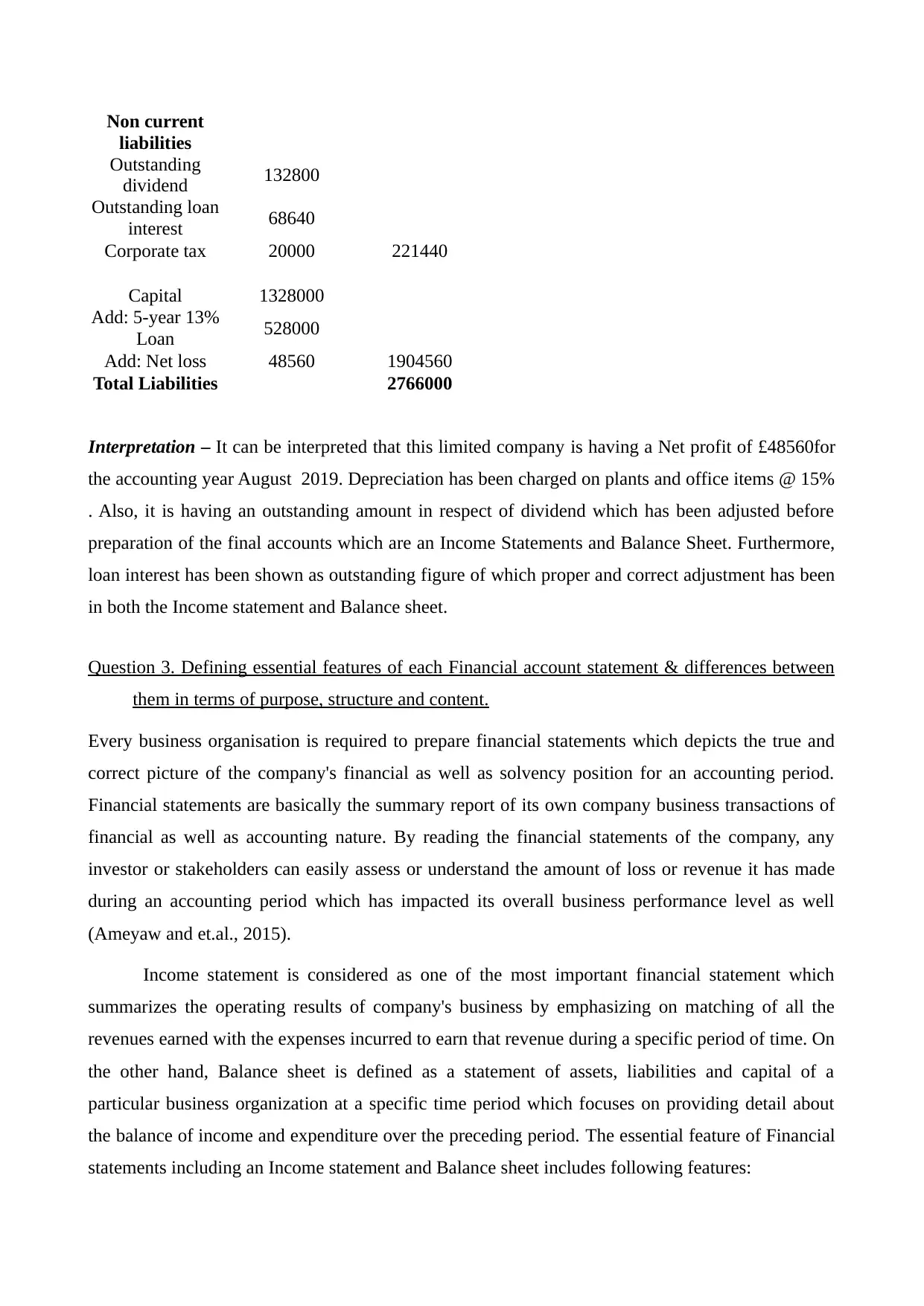

Total Assets 2766000

Current

liabilities

Trade payables 640000 640000

Non current

liabilities

Outstanding

dividend 132800

Outstanding loan

interest 68640

Corporate tax 20000 221440

Capital 1328000

Add: 5-year 13%

Loan 528000

Add: Net loss 48560 1904560

Total Liabilities 2766000

1. Depreciation on Plant and equipment.

Particulars Amount (£)

Plant and

equipment 768000

Particulars Amount (£) Amount (£)

Fixed Assets

Leasehold

Premises 1232000

Office Furniture 163200

Plant and

Equipment 652800 2048000

Current Assets

Trade receivables 608000

Inventory 78000

Bank 32000 718000

Total Assets 2766000

Current

liabilities

Trade payables 640000 640000

Non current

liabilities

Outstanding

dividend 132800

Outstanding loan

interest 68640

Corporate tax 20000 221440

Capital 1328000

Add: 5-year 13%

Loan 528000

Add: Net loss 48560 1904560

Total Liabilities 2766000

1. Depreciation on Plant and equipment.

Particulars Amount (£)

Plant and

equipment 768000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Depreciation 15.00%

Less:

Depreciation

amount

115200

Plant and

equipment 652800

2. Depreciation on Office equipment.

Particulars Amount (£)

Office equipment 192000

Depreciation 15.00%

Less:

Depreciation

amount

28800

Office

equipment 163200

Interpretation – It can be interpreted that the partnership is having a Net profit of £48560for the

accounting year August 2019. Depreciation has been charged on plants and office items @ 15% .

Also, it is having an outstanding amount in respect of dividend which has been adjusted before

preparation of the final accounts which are an Income Statements and Balance Sheet. Furthermore,

loan interest has been shown as outstanding figure of which proper and correct adjustment has been

in both the Income statement and Balance sheet of this partnership firm.

3. Limited company – It is a type of private company in which owners are held personally liable

for all the debts and liabilities up to the capital amount invested by them.

Final account of Limited company

Income statement for the year ended 31st August 2019 of Kenny Paton Ltd

Particulars Amount (£) Amount (£)

Sales 2064000

Less: Sales

returns 0

Net sales 2064000 2064000

Less: Cost of

sales

Opening

inventory 96000

Purchases 1024000

Purchases returns 0 1120000

Add: Closing 78000 78000

Less:

Depreciation

amount

115200

Plant and

equipment 652800

2. Depreciation on Office equipment.

Particulars Amount (£)

Office equipment 192000

Depreciation 15.00%

Less:

Depreciation

amount

28800

Office

equipment 163200

Interpretation – It can be interpreted that the partnership is having a Net profit of £48560for the

accounting year August 2019. Depreciation has been charged on plants and office items @ 15% .

Also, it is having an outstanding amount in respect of dividend which has been adjusted before

preparation of the final accounts which are an Income Statements and Balance Sheet. Furthermore,

loan interest has been shown as outstanding figure of which proper and correct adjustment has been

in both the Income statement and Balance sheet of this partnership firm.

3. Limited company – It is a type of private company in which owners are held personally liable

for all the debts and liabilities up to the capital amount invested by them.

Final account of Limited company

Income statement for the year ended 31st August 2019 of Kenny Paton Ltd

Particulars Amount (£) Amount (£)

Sales 2064000

Less: Sales

returns 0

Net sales 2064000 2064000

Less: Cost of

sales

Opening

inventory 96000

Purchases 1024000

Purchases returns 0 1120000

Add: Closing 78000 78000

inventory

Gross profit 1022000

Add: Outstanding

loan interest 68640

Outstanding

dividend 132800 201440

Less: Expenses

Distribution costs 336000

Corporation tax 20000

Administration

costs 272000 628000

Depreciation:

Plant and

equipment 115200

Office equipment 28800 144000

Total 973440

Net loss 48560

Statement of financial position at the year ended 31st August 2019 of Kenny Paton Ltd

Particulars Amount (£) Amount (£)

Fixed Assets

Leasehold

Premises 1232000

Office Furniture 163200

Plant and

Equipment 652800 2048000

Current Assets

Trade receivables 608000

Inventory 78000

Bank 32000 718000

Total Assets 2766000

Current

liabilities

Trade payables 640000 640000

Gross profit 1022000

Add: Outstanding

loan interest 68640

Outstanding

dividend 132800 201440

Less: Expenses

Distribution costs 336000

Corporation tax 20000

Administration

costs 272000 628000

Depreciation:

Plant and

equipment 115200

Office equipment 28800 144000

Total 973440

Net loss 48560

Statement of financial position at the year ended 31st August 2019 of Kenny Paton Ltd

Particulars Amount (£) Amount (£)

Fixed Assets

Leasehold

Premises 1232000

Office Furniture 163200

Plant and

Equipment 652800 2048000

Current Assets

Trade receivables 608000

Inventory 78000

Bank 32000 718000

Total Assets 2766000

Current

liabilities

Trade payables 640000 640000

Non current

liabilities

Outstanding

dividend 132800

Outstanding loan

interest 68640

Corporate tax 20000 221440

Capital 1328000

Add: 5-year 13%

Loan 528000

Add: Net loss 48560 1904560

Total Liabilities 2766000

Interpretation – It can be interpreted that this limited company is having a Net profit of £48560for

the accounting year August 2019. Depreciation has been charged on plants and office items @ 15%

. Also, it is having an outstanding amount in respect of dividend which has been adjusted before

preparation of the final accounts which are an Income Statements and Balance Sheet. Furthermore,

loan interest has been shown as outstanding figure of which proper and correct adjustment has been

in both the Income statement and Balance sheet.

Question 3. Defining essential features of each Financial account statement & differences between

them in terms of purpose, structure and content.

Every business organisation is required to prepare financial statements which depicts the true and

correct picture of the company's financial as well as solvency position for an accounting period.

Financial statements are basically the summary report of its own company business transactions of

financial as well as accounting nature. By reading the financial statements of the company, any

investor or stakeholders can easily assess or understand the amount of loss or revenue it has made

during an accounting period which has impacted its overall business performance level as well

(Ameyaw and et.al., 2015).

Income statement is considered as one of the most important financial statement which

summarizes the operating results of company's business by emphasizing on matching of all the

revenues earned with the expenses incurred to earn that revenue during a specific period of time. On

the other hand, Balance sheet is defined as a statement of assets, liabilities and capital of a

particular business organization at a specific time period which focuses on providing detail about

the balance of income and expenditure over the preceding period. The essential feature of Financial

statements including an Income statement and Balance sheet includes following features:

liabilities

Outstanding

dividend 132800

Outstanding loan

interest 68640

Corporate tax 20000 221440

Capital 1328000

Add: 5-year 13%

Loan 528000

Add: Net loss 48560 1904560

Total Liabilities 2766000

Interpretation – It can be interpreted that this limited company is having a Net profit of £48560for

the accounting year August 2019. Depreciation has been charged on plants and office items @ 15%

. Also, it is having an outstanding amount in respect of dividend which has been adjusted before

preparation of the final accounts which are an Income Statements and Balance Sheet. Furthermore,

loan interest has been shown as outstanding figure of which proper and correct adjustment has been

in both the Income statement and Balance sheet.

Question 3. Defining essential features of each Financial account statement & differences between

them in terms of purpose, structure and content.

Every business organisation is required to prepare financial statements which depicts the true and

correct picture of the company's financial as well as solvency position for an accounting period.

Financial statements are basically the summary report of its own company business transactions of

financial as well as accounting nature. By reading the financial statements of the company, any

investor or stakeholders can easily assess or understand the amount of loss or revenue it has made

during an accounting period which has impacted its overall business performance level as well

(Ameyaw and et.al., 2015).

Income statement is considered as one of the most important financial statement which

summarizes the operating results of company's business by emphasizing on matching of all the

revenues earned with the expenses incurred to earn that revenue during a specific period of time. On

the other hand, Balance sheet is defined as a statement of assets, liabilities and capital of a

particular business organization at a specific time period which focuses on providing detail about

the balance of income and expenditure over the preceding period. The essential feature of Financial

statements including an Income statement and Balance sheet includes following features:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

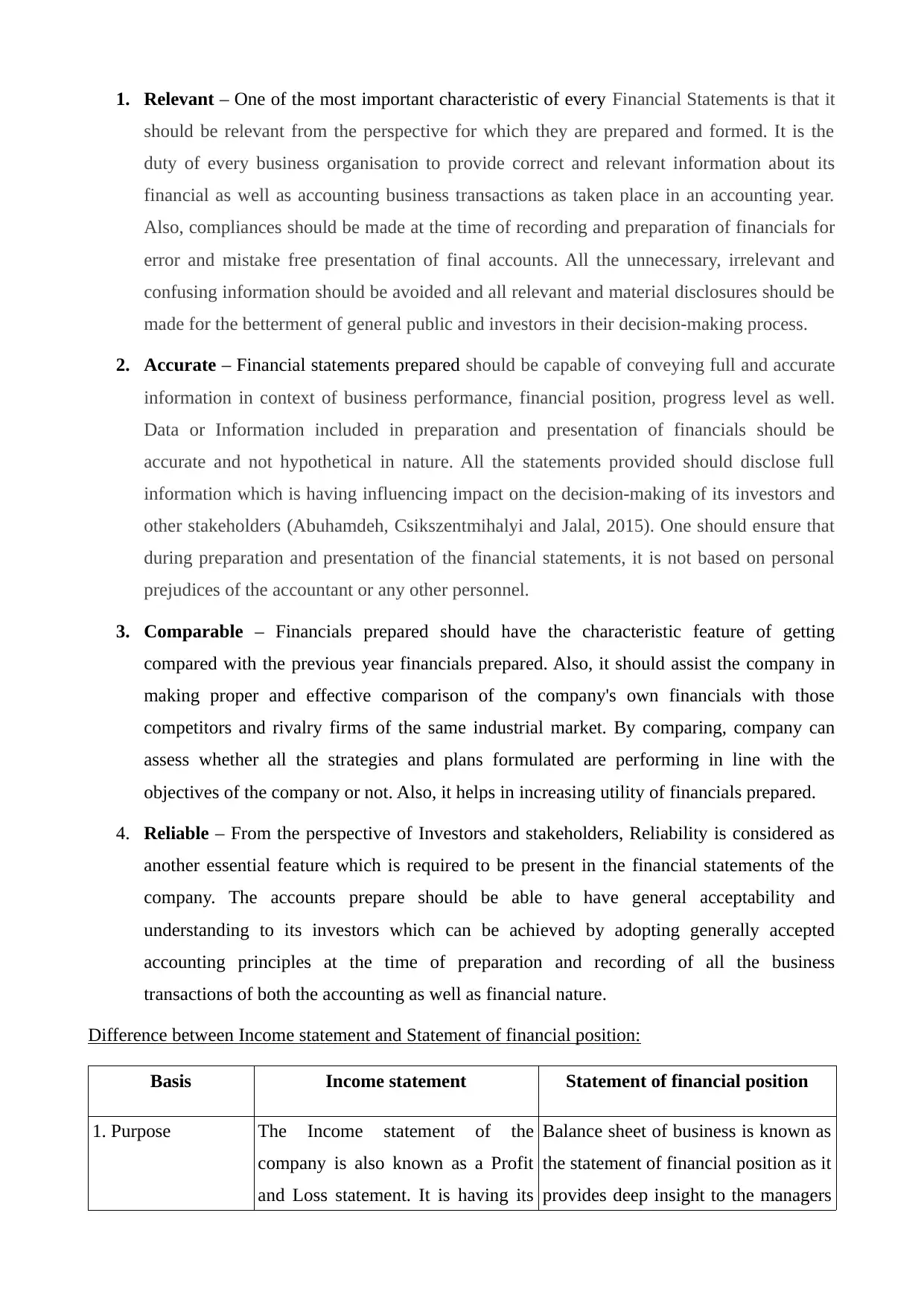

1. Relevant – One of the most important characteristic of every Financial Statements is that it

should be relevant from the perspective for which they are prepared and formed. It is the

duty of every business organisation to provide correct and relevant information about its

financial as well as accounting business transactions as taken place in an accounting year.

Also, compliances should be made at the time of recording and preparation of financials for

error and mistake free presentation of final accounts. All the unnecessary, irrelevant and

confusing information should be avoided and all relevant and material disclosures should be

made for the betterment of general public and investors in their decision-making process.

2. Accurate – Financial statements prepared should be capable of conveying full and accurate

information in context of business performance, financial position, progress level as well.

Data or Information included in preparation and presentation of financials should be

accurate and not hypothetical in nature. All the statements provided should disclose full

information which is having influencing impact on the decision-making of its investors and

other stakeholders (Abuhamdeh, Csikszentmihalyi and Jalal, 2015). One should ensure that

during preparation and presentation of the financial statements, it is not based on personal

prejudices of the accountant or any other personnel.

3. Comparable – Financials prepared should have the characteristic feature of getting

compared with the previous year financials prepared. Also, it should assist the company in

making proper and effective comparison of the company's own financials with those

competitors and rivalry firms of the same industrial market. By comparing, company can

assess whether all the strategies and plans formulated are performing in line with the

objectives of the company or not. Also, it helps in increasing utility of financials prepared.

4. Reliable – From the perspective of Investors and stakeholders, Reliability is considered as

another essential feature which is required to be present in the financial statements of the

company. The accounts prepare should be able to have general acceptability and

understanding to its investors which can be achieved by adopting generally accepted

accounting principles at the time of preparation and recording of all the business

transactions of both the accounting as well as financial nature.

Difference between Income statement and Statement of financial position:

Basis Income statement Statement of financial position

1. Purpose The Income statement of the

company is also known as a Profit

and Loss statement. It is having its

Balance sheet of business is known as

the statement of financial position as it

provides deep insight to the managers

should be relevant from the perspective for which they are prepared and formed. It is the

duty of every business organisation to provide correct and relevant information about its

financial as well as accounting business transactions as taken place in an accounting year.

Also, compliances should be made at the time of recording and preparation of financials for

error and mistake free presentation of final accounts. All the unnecessary, irrelevant and

confusing information should be avoided and all relevant and material disclosures should be

made for the betterment of general public and investors in their decision-making process.

2. Accurate – Financial statements prepared should be capable of conveying full and accurate

information in context of business performance, financial position, progress level as well.

Data or Information included in preparation and presentation of financials should be

accurate and not hypothetical in nature. All the statements provided should disclose full

information which is having influencing impact on the decision-making of its investors and

other stakeholders (Abuhamdeh, Csikszentmihalyi and Jalal, 2015). One should ensure that

during preparation and presentation of the financial statements, it is not based on personal

prejudices of the accountant or any other personnel.

3. Comparable – Financials prepared should have the characteristic feature of getting

compared with the previous year financials prepared. Also, it should assist the company in

making proper and effective comparison of the company's own financials with those

competitors and rivalry firms of the same industrial market. By comparing, company can

assess whether all the strategies and plans formulated are performing in line with the

objectives of the company or not. Also, it helps in increasing utility of financials prepared.

4. Reliable – From the perspective of Investors and stakeholders, Reliability is considered as

another essential feature which is required to be present in the financial statements of the

company. The accounts prepare should be able to have general acceptability and

understanding to its investors which can be achieved by adopting generally accepted

accounting principles at the time of preparation and recording of all the business

transactions of both the accounting as well as financial nature.

Difference between Income statement and Statement of financial position:

Basis Income statement Statement of financial position

1. Purpose The Income statement of the

company is also known as a Profit

and Loss statement. It is having its

Balance sheet of business is known as

the statement of financial position as it

provides deep insight to the managers

primary purpose to evaluate and

determine how much money a

company has earned or lost over a

specified time period (Madhavi,

2017). It is very easy for both the

internal as well as external users to

identify main sources of profits and

losses as the income statement

provides detailed breakdown of its

earnings and expenses down into

different categories.

and investors of the company related

to overview of company's financial

positions. It defines where the

company is at the present level and

what is its liquidity as well as

solvency position.

2. Content The income statement is a document

which has all information pertaining

to business's income and expenses

over a specific period of time.

Revenue is shown on the credit side

on the income statement whereas

expenses are recorded on debit side.

The balance sheet depicts true and

correct image of company's position.

It is defined in form of financial report

emphasizing mainly on three items

viz. Assets, liabilities and owners'

equity. The Assets are those properties

which are owned by the company,

liabilities are the financial obligations

of the company and owners' equity is

the value of the company to its

shareholders.

3. Structure The Income statement equation

defines how the income has been

derived from the period's revenues

and expenses i.e. Income =

Revenues – Expenses.

This statement also perform function

of adding and subtracting some of

these figures so as to show profits

which are Gross profit, Operating

profit and Net profit for an

accounting period.

The Balance sheet of company shows

the following financial and accounting

information about the company:

1. Total Assets - Item of value the firm

has owned or controlled which is used

by the company to earn revenues.

2. Total Liabilities - What is the

amount of money which the firm has

owes (Pollin, Downey Jr and Fleming,

Autoscribe Corp, 2017).

3. Total Owners Equities – What is the

determine how much money a

company has earned or lost over a

specified time period (Madhavi,

2017). It is very easy for both the

internal as well as external users to

identify main sources of profits and

losses as the income statement

provides detailed breakdown of its

earnings and expenses down into

different categories.

and investors of the company related

to overview of company's financial

positions. It defines where the

company is at the present level and

what is its liquidity as well as

solvency position.

2. Content The income statement is a document

which has all information pertaining

to business's income and expenses

over a specific period of time.

Revenue is shown on the credit side

on the income statement whereas

expenses are recorded on debit side.

The balance sheet depicts true and

correct image of company's position.

It is defined in form of financial report

emphasizing mainly on three items

viz. Assets, liabilities and owners'

equity. The Assets are those properties

which are owned by the company,

liabilities are the financial obligations

of the company and owners' equity is

the value of the company to its

shareholders.

3. Structure The Income statement equation

defines how the income has been

derived from the period's revenues

and expenses i.e. Income =

Revenues – Expenses.

This statement also perform function

of adding and subtracting some of

these figures so as to show profits

which are Gross profit, Operating

profit and Net profit for an

accounting period.

The Balance sheet of company shows

the following financial and accounting

information about the company:

1. Total Assets - Item of value the firm

has owned or controlled which is used

by the company to earn revenues.

2. Total Liabilities - What is the

amount of money which the firm has

owes (Pollin, Downey Jr and Fleming,

Autoscribe Corp, 2017).

3. Total Owners Equities – What is the

amount which the firm has owns

outright.

Question 4. Defining the process of bank reconciliation statement and its usage in checking general

accounts and balance sheets.

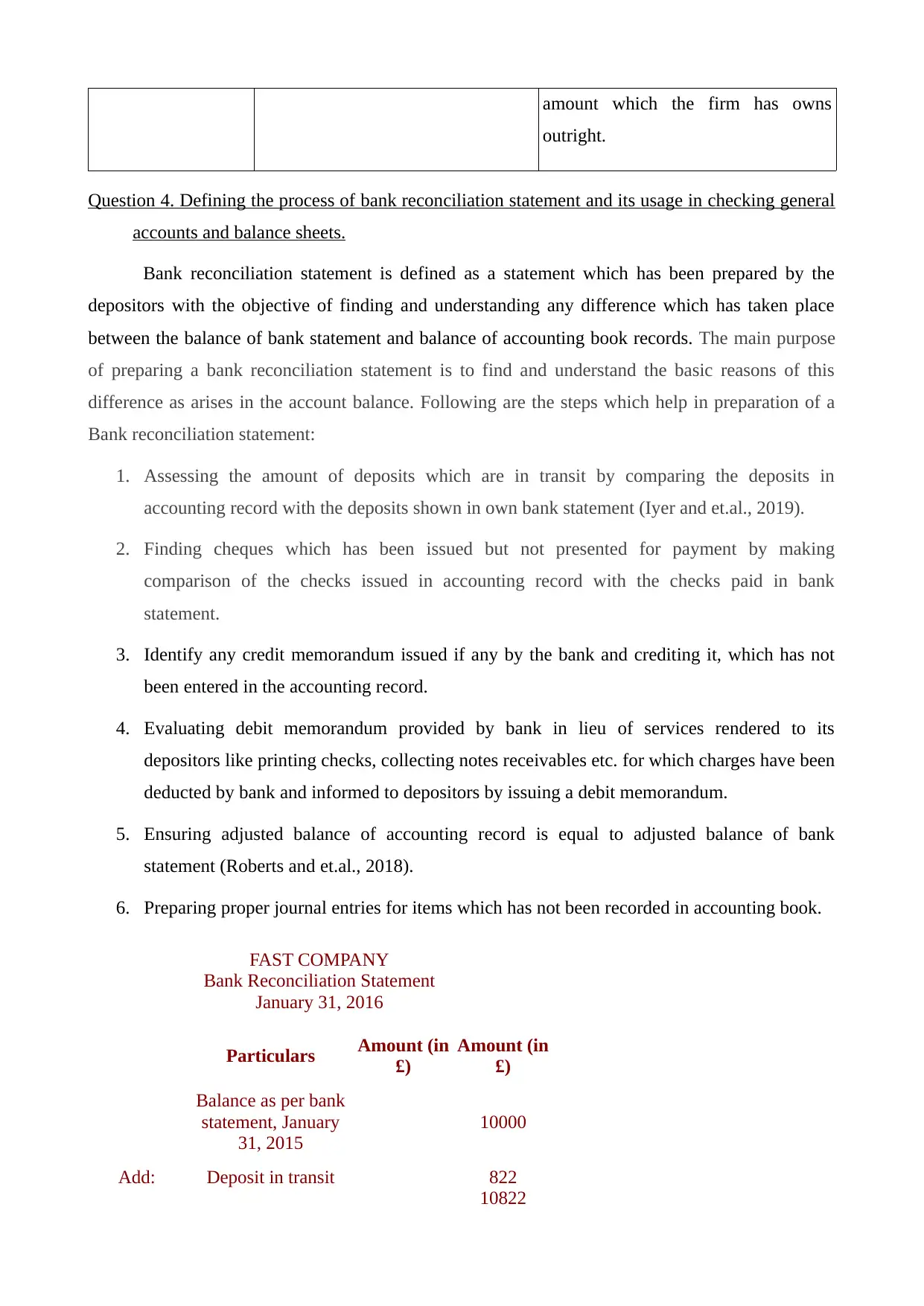

Bank reconciliation statement is defined as a statement which has been prepared by the

depositors with the objective of finding and understanding any difference which has taken place

between the balance of bank statement and balance of accounting book records. The main purpose

of preparing a bank reconciliation statement is to find and understand the basic reasons of this

difference as arises in the account balance. Following are the steps which help in preparation of a

Bank reconciliation statement:

1. Assessing the amount of deposits which are in transit by comparing the deposits in

accounting record with the deposits shown in own bank statement (Iyer and et.al., 2019).

2. Finding cheques which has been issued but not presented for payment by making

comparison of the checks issued in accounting record with the checks paid in bank

statement.

3. Identify any credit memorandum issued if any by the bank and crediting it, which has not

been entered in the accounting record.

4. Evaluating debit memorandum provided by bank in lieu of services rendered to its

depositors like printing checks, collecting notes receivables etc. for which charges have been

deducted by bank and informed to depositors by issuing a debit memorandum.

5. Ensuring adjusted balance of accounting record is equal to adjusted balance of bank

statement (Roberts and et.al., 2018).

6. Preparing proper journal entries for items which has not been recorded in accounting book.

FAST COMPANY

Bank Reconciliation Statement

January 31, 2016

Particulars Amount (in

£)

Amount (in

£)

Balance as per bank

statement, January

31, 2015

10000

Add: Deposit in transit 822

10822

outright.

Question 4. Defining the process of bank reconciliation statement and its usage in checking general

accounts and balance sheets.

Bank reconciliation statement is defined as a statement which has been prepared by the

depositors with the objective of finding and understanding any difference which has taken place

between the balance of bank statement and balance of accounting book records. The main purpose

of preparing a bank reconciliation statement is to find and understand the basic reasons of this

difference as arises in the account balance. Following are the steps which help in preparation of a

Bank reconciliation statement:

1. Assessing the amount of deposits which are in transit by comparing the deposits in

accounting record with the deposits shown in own bank statement (Iyer and et.al., 2019).

2. Finding cheques which has been issued but not presented for payment by making

comparison of the checks issued in accounting record with the checks paid in bank

statement.

3. Identify any credit memorandum issued if any by the bank and crediting it, which has not

been entered in the accounting record.

4. Evaluating debit memorandum provided by bank in lieu of services rendered to its

depositors like printing checks, collecting notes receivables etc. for which charges have been

deducted by bank and informed to depositors by issuing a debit memorandum.

5. Ensuring adjusted balance of accounting record is equal to adjusted balance of bank

statement (Roberts and et.al., 2018).

6. Preparing proper journal entries for items which has not been recorded in accounting book.

FAST COMPANY

Bank Reconciliation Statement

January 31, 2016

Particulars Amount (in

£)

Amount (in

£)

Balance as per bank

statement, January

31, 2015

10000

Add: Deposit in transit 822

10822

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

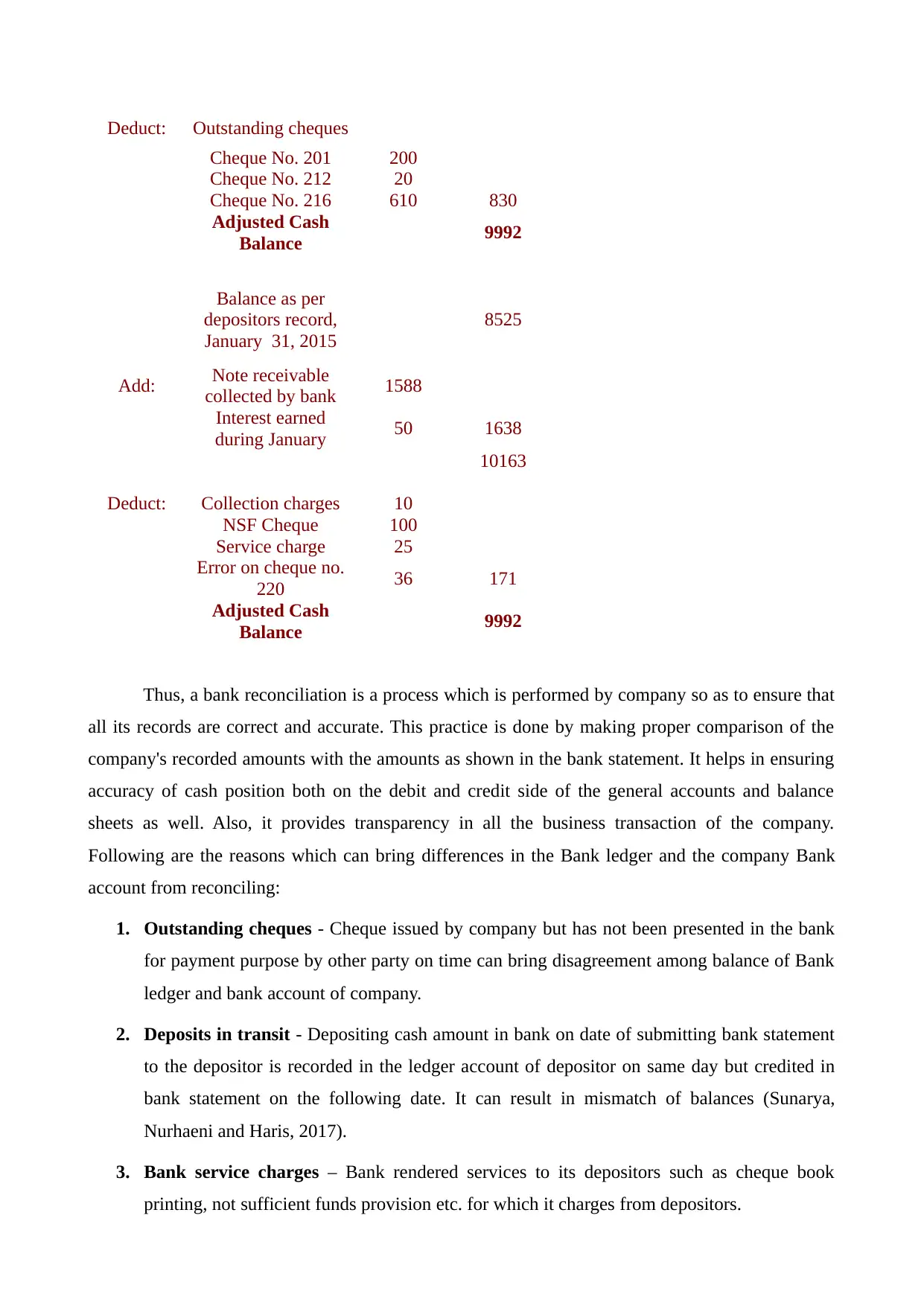

Deduct: Outstanding cheques

Cheque No. 201 200

Cheque No. 212 20

Cheque No. 216 610 830

Adjusted Cash

Balance 9992

Balance as per

depositors record,

January 31, 2015

8525

Add: Note receivable

collected by bank 1588

Interest earned

during January 50 1638

10163

Deduct: Collection charges 10

NSF Cheque 100

Service charge 25

Error on cheque no.

220 36 171

Adjusted Cash

Balance 9992

Thus, a bank reconciliation is a process which is performed by company so as to ensure that

all its records are correct and accurate. This practice is done by making proper comparison of the

company's recorded amounts with the amounts as shown in the bank statement. It helps in ensuring

accuracy of cash position both on the debit and credit side of the general accounts and balance

sheets as well. Also, it provides transparency in all the business transaction of the company.

Following are the reasons which can bring differences in the Bank ledger and the company Bank

account from reconciling:

1. Outstanding cheques - Cheque issued by company but has not been presented in the bank

for payment purpose by other party on time can bring disagreement among balance of Bank

ledger and bank account of company.

2. Deposits in transit - Depositing cash amount in bank on date of submitting bank statement

to the depositor is recorded in the ledger account of depositor on same day but credited in

bank statement on the following date. It can result in mismatch of balances (Sunarya,

Nurhaeni and Haris, 2017).

3. Bank service charges – Bank rendered services to its depositors such as cheque book

printing, not sufficient funds provision etc. for which it charges from depositors.

Cheque No. 201 200

Cheque No. 212 20

Cheque No. 216 610 830

Adjusted Cash

Balance 9992

Balance as per

depositors record,

January 31, 2015

8525

Add: Note receivable

collected by bank 1588

Interest earned

during January 50 1638

10163

Deduct: Collection charges 10

NSF Cheque 100

Service charge 25

Error on cheque no.

220 36 171

Adjusted Cash

Balance 9992

Thus, a bank reconciliation is a process which is performed by company so as to ensure that

all its records are correct and accurate. This practice is done by making proper comparison of the

company's recorded amounts with the amounts as shown in the bank statement. It helps in ensuring

accuracy of cash position both on the debit and credit side of the general accounts and balance

sheets as well. Also, it provides transparency in all the business transaction of the company.

Following are the reasons which can bring differences in the Bank ledger and the company Bank

account from reconciling:

1. Outstanding cheques - Cheque issued by company but has not been presented in the bank

for payment purpose by other party on time can bring disagreement among balance of Bank

ledger and bank account of company.

2. Deposits in transit - Depositing cash amount in bank on date of submitting bank statement

to the depositor is recorded in the ledger account of depositor on same day but credited in

bank statement on the following date. It can result in mismatch of balances (Sunarya,

Nurhaeni and Haris, 2017).

3. Bank service charges – Bank rendered services to its depositors such as cheque book

printing, not sufficient funds provision etc. for which it charges from depositors.

4. Errors in the books – Any wrong entry or recording has been made by the depositors by

mistakenly in owns books of accounts can result in disagreement.

5. Errors by the bank – If bank made any deposits or credit in the depositors bank account

erroneously, then mismatch will remain till correction are not made.

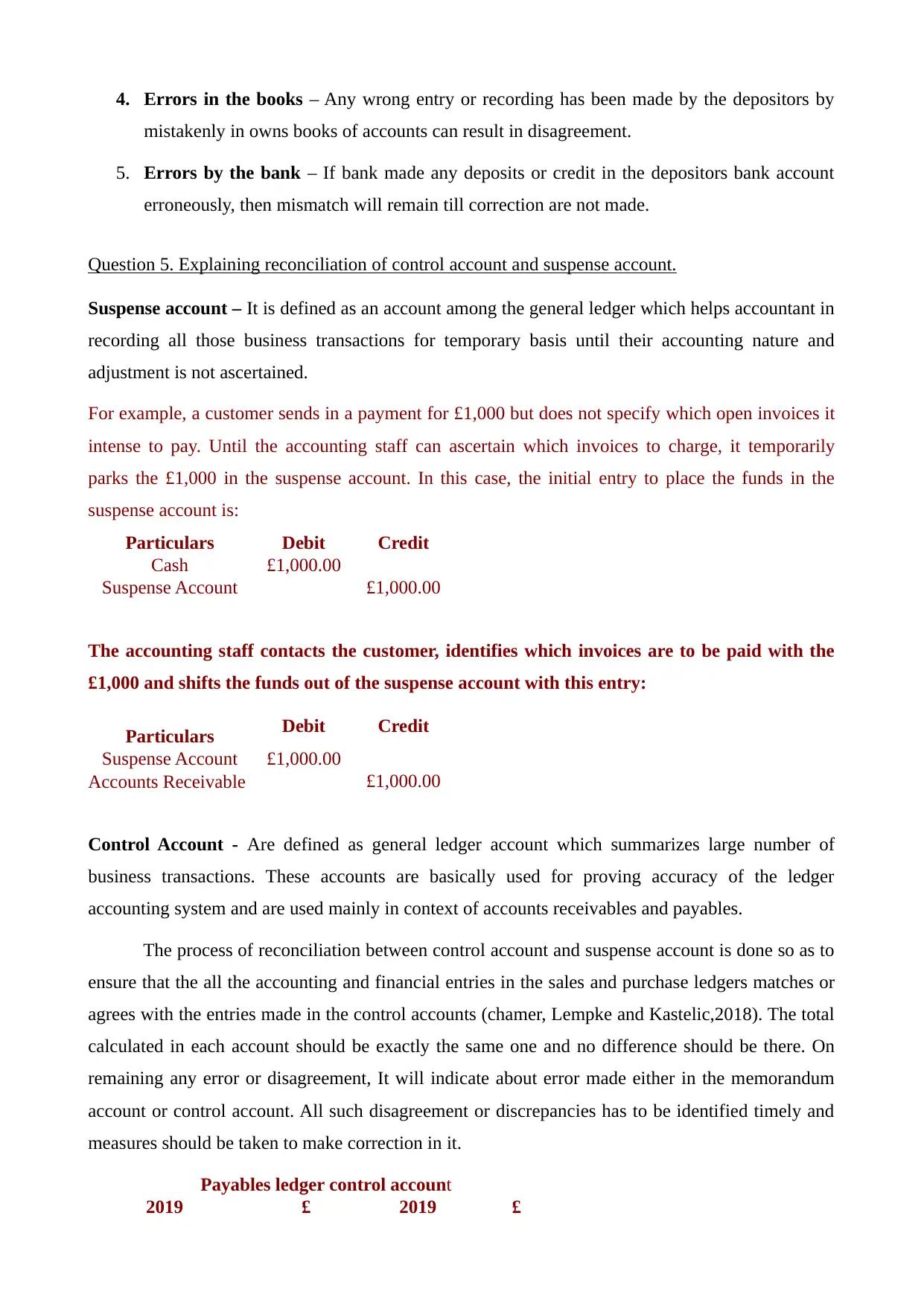

Question 5. Explaining reconciliation of control account and suspense account.

Suspense account – It is defined as an account among the general ledger which helps accountant in

recording all those business transactions for temporary basis until their accounting nature and

adjustment is not ascertained.

For example, a customer sends in a payment for £1,000 but does not specify which open invoices it

intense to pay. Until the accounting staff can ascertain which invoices to charge, it temporarily

parks the £1,000 in the suspense account. In this case, the initial entry to place the funds in the

suspense account is:

Particulars Debit Credit

Cash £1,000.00

Suspense Account £1,000.00

The accounting staff contacts the customer, identifies which invoices are to be paid with the

£1,000 and shifts the funds out of the suspense account with this entry:

Particulars Debit Credit

Suspense Account £1,000.00

Accounts Receivable £1,000.00

Control Account - Are defined as general ledger account which summarizes large number of

business transactions. These accounts are basically used for proving accuracy of the ledger

accounting system and are used mainly in context of accounts receivables and payables.

The process of reconciliation between control account and suspense account is done so as to

ensure that the all the accounting and financial entries in the sales and purchase ledgers matches or

agrees with the entries made in the control accounts (chamer, Lempke and Kastelic,2018). The total

calculated in each account should be exactly the same one and no difference should be there. On

remaining any error or disagreement, It will indicate about error made either in the memorandum

account or control account. All such disagreement or discrepancies has to be identified timely and

measures should be taken to make correction in it.

Payables ledger control account

2019 £ 2019 £

mistakenly in owns books of accounts can result in disagreement.

5. Errors by the bank – If bank made any deposits or credit in the depositors bank account

erroneously, then mismatch will remain till correction are not made.

Question 5. Explaining reconciliation of control account and suspense account.

Suspense account – It is defined as an account among the general ledger which helps accountant in

recording all those business transactions for temporary basis until their accounting nature and

adjustment is not ascertained.

For example, a customer sends in a payment for £1,000 but does not specify which open invoices it

intense to pay. Until the accounting staff can ascertain which invoices to charge, it temporarily

parks the £1,000 in the suspense account. In this case, the initial entry to place the funds in the

suspense account is:

Particulars Debit Credit

Cash £1,000.00

Suspense Account £1,000.00

The accounting staff contacts the customer, identifies which invoices are to be paid with the

£1,000 and shifts the funds out of the suspense account with this entry:

Particulars Debit Credit

Suspense Account £1,000.00

Accounts Receivable £1,000.00

Control Account - Are defined as general ledger account which summarizes large number of

business transactions. These accounts are basically used for proving accuracy of the ledger

accounting system and are used mainly in context of accounts receivables and payables.

The process of reconciliation between control account and suspense account is done so as to

ensure that the all the accounting and financial entries in the sales and purchase ledgers matches or

agrees with the entries made in the control accounts (chamer, Lempke and Kastelic,2018). The total

calculated in each account should be exactly the same one and no difference should be there. On

remaining any error or disagreement, It will indicate about error made either in the memorandum

account or control account. All such disagreement or discrepancies has to be identified timely and

measures should be taken to make correction in it.

Payables ledger control account

2019 £ 2019 £

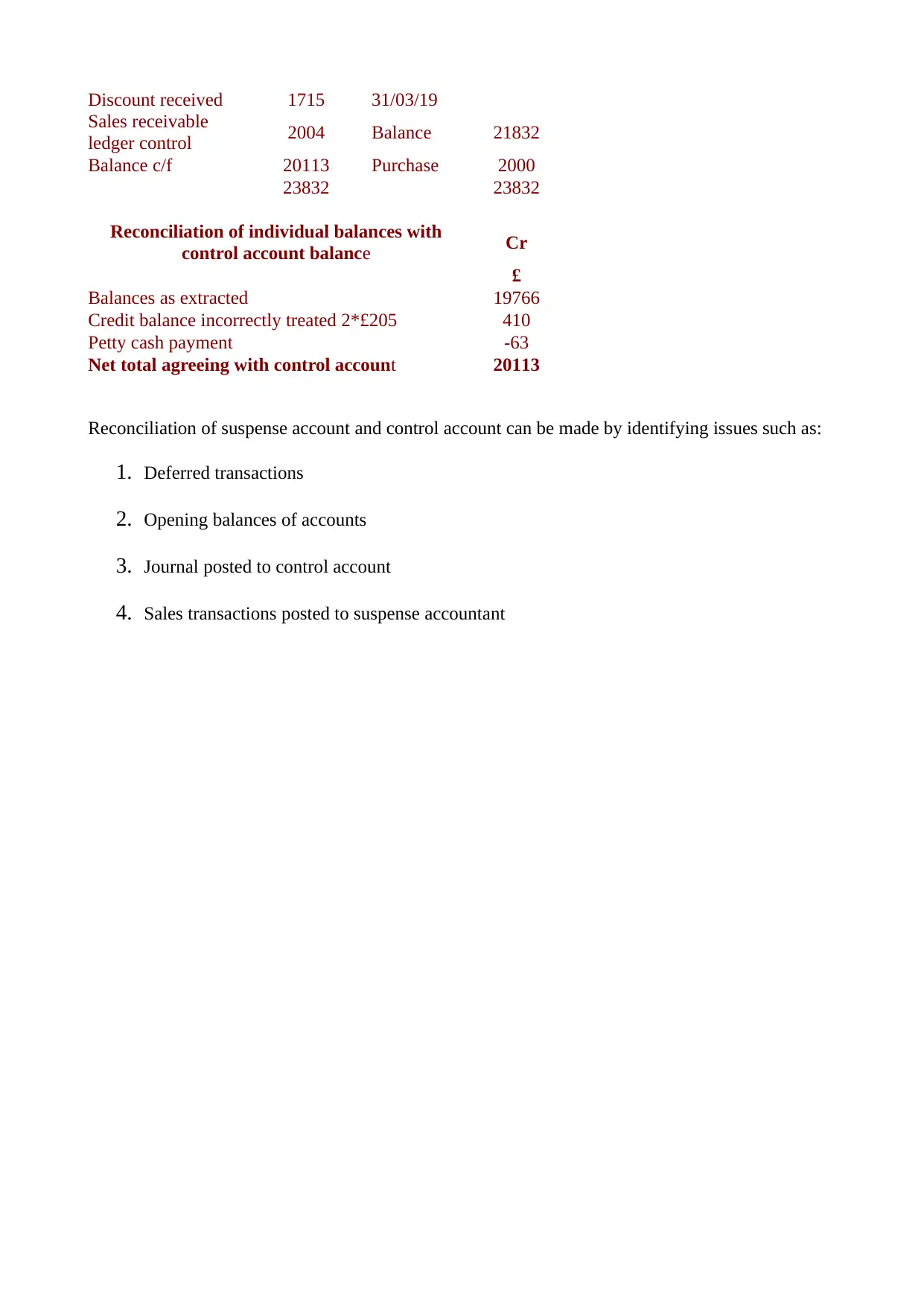

Discount received 1715 31/03/19

Sales receivable

ledger control 2004 Balance 21832

Balance c/f 20113 Purchase 2000

23832 23832

Reconciliation of individual balances with

control account balance Cr

£

Balances as extracted 19766

Credit balance incorrectly treated 2*£205 410

Petty cash payment -63

Net total agreeing with control account 20113

Reconciliation of suspense account and control account can be made by identifying issues such as:

1. Deferred transactions

2. Opening balances of accounts

3. Journal posted to control account

4. Sales transactions posted to suspense accountant

Sales receivable

ledger control 2004 Balance 21832

Balance c/f 20113 Purchase 2000

23832 23832

Reconciliation of individual balances with

control account balance Cr

£

Balances as extracted 19766

Credit balance incorrectly treated 2*£205 410

Petty cash payment -63

Net total agreeing with control account 20113

Reconciliation of suspense account and control account can be made by identifying issues such as:

1. Deferred transactions

2. Opening balances of accounts

3. Journal posted to control account

4. Sales transactions posted to suspense accountant

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONCLUSION

From the above report it can be concluded that by adopting sound and effective financial and

accounting policies and guidelines, every business organisation can deliver true and accurate

financial information to its internal as well as external business users such as managers, investors,

government, stakeholders, competitors etc. The report has contained financial statement such as an

Income statement and balance sheet prepared for sole traders, partnership business and limited

company. Further, it has been observed that bank reconciliation process helps in assessing all the

discrepancies which has been arises in the recording and preparation process of the company's

financial statements. It helps depositors and company in assessing reason for disagreement between

the balances of bank account and accounting record book of the company. At last, the report has

elaborate about suspense account and its meaning i.e. such accounts helps accountant in making

adjustment of that business and financial transaction of which the accounting nature has not been

ascertained at the time of making entries. Whereas control accounts is that account which can be

used for recording all the balances arises on a number of subsidiary accounts so as to provide a

cross check on these business transactions.

From the above report it can be concluded that by adopting sound and effective financial and

accounting policies and guidelines, every business organisation can deliver true and accurate

financial information to its internal as well as external business users such as managers, investors,

government, stakeholders, competitors etc. The report has contained financial statement such as an

Income statement and balance sheet prepared for sole traders, partnership business and limited

company. Further, it has been observed that bank reconciliation process helps in assessing all the

discrepancies which has been arises in the recording and preparation process of the company's

financial statements. It helps depositors and company in assessing reason for disagreement between

the balances of bank account and accounting record book of the company. At last, the report has

elaborate about suspense account and its meaning i.e. such accounts helps accountant in making

adjustment of that business and financial transaction of which the accounting nature has not been

ascertained at the time of making entries. Whereas control accounts is that account which can be

used for recording all the balances arises on a number of subsidiary accounts so as to provide a

cross check on these business transactions.

REFERENCES

Books and Journals

Abuhamdeh, S., Csikszentmihalyi, M. and Jalal, B., 2015. Enjoying the possibility of defeat:

Outcome uncertainty, suspense, and intrinsic motivation. Motivation and Emotion. 39(1). pp.1-

10.

Ameyaw, E. E. and et.al., 2015. A fuzzy model for evaluating risk impacts on variability between

contract sum and final account in government-funded construction projects. Journal of

Facilities Management. 13(1). pp.45-69.

Iyer, N. and et.al., 2019. Bank Reconciliation Bot. Available at SSRN 3370760.

Madhavi, A., 2017. BANK STATEMENTS RECONCILIATION USING SWIFT-MESSAGE

TRANSFER940. Journal of Global Research in Computer Science. 8(10). pp.05-09.

Pollin, R. E., Downey Jr, B. E. and Fleming, S. A., Autoscribe Corp, 2017. System and method for

registering financial accounts. U.S. Patent Application 15/408.185.

Roberts, D. and et.al., Connectyourcare LLC, 2018. Reconciliation for enabling accelerated access

to contribution funded accounts. U.S. Patent Application 16/039.188.

Schamer, D., Lempke, L. and Kastelic, J., Huntington Bancshares Inc, 2017. System and Method

for Providing Time to Cure Negative Balances in Financial Accounts While Encouraging Rapid

Curing of Those Balances to a Positive Net Position. U.S. Patent Application 15/262.524.

Schamer, D., Lempke, L. and Kastelic, J., Huntington Bancshares Inc, 2018. System and Method

for Providing Time to Cure Negative Balances in Financial Accounts While Encouraging Rapid

Curing of Those Balances to a Positive Net Position. U.S. Patent Application 15/720.590.

Sunarya, P. A., Nurhaeni, T. and Haris, H., 2017. Bank Reconciliation Process Efficiency Using

Online Web Based Accounting System 2.0 in Companies. Aptisi Transactions On Management.

1(2). pp.124-129.

Online

Difference Between Income Statement & Balance Sheets. 2019. [Online]. Available through:

<https://smallbusiness.chron.com/difference-between-income-statement-balance-sheets-

55419.html>.

Features of Financial Statements. 2019. [Online]. Available through:

<http://www.yourarticlelibrary.com/accounting/financial-statements/financial-statements-

Books and Journals

Abuhamdeh, S., Csikszentmihalyi, M. and Jalal, B., 2015. Enjoying the possibility of defeat:

Outcome uncertainty, suspense, and intrinsic motivation. Motivation and Emotion. 39(1). pp.1-

10.

Ameyaw, E. E. and et.al., 2015. A fuzzy model for evaluating risk impacts on variability between

contract sum and final account in government-funded construction projects. Journal of

Facilities Management. 13(1). pp.45-69.

Iyer, N. and et.al., 2019. Bank Reconciliation Bot. Available at SSRN 3370760.

Madhavi, A., 2017. BANK STATEMENTS RECONCILIATION USING SWIFT-MESSAGE

TRANSFER940. Journal of Global Research in Computer Science. 8(10). pp.05-09.

Pollin, R. E., Downey Jr, B. E. and Fleming, S. A., Autoscribe Corp, 2017. System and method for

registering financial accounts. U.S. Patent Application 15/408.185.

Roberts, D. and et.al., Connectyourcare LLC, 2018. Reconciliation for enabling accelerated access

to contribution funded accounts. U.S. Patent Application 16/039.188.

Schamer, D., Lempke, L. and Kastelic, J., Huntington Bancshares Inc, 2017. System and Method

for Providing Time to Cure Negative Balances in Financial Accounts While Encouraging Rapid

Curing of Those Balances to a Positive Net Position. U.S. Patent Application 15/262.524.

Schamer, D., Lempke, L. and Kastelic, J., Huntington Bancshares Inc, 2018. System and Method

for Providing Time to Cure Negative Balances in Financial Accounts While Encouraging Rapid

Curing of Those Balances to a Positive Net Position. U.S. Patent Application 15/720.590.

Sunarya, P. A., Nurhaeni, T. and Haris, H., 2017. Bank Reconciliation Process Efficiency Using

Online Web Based Accounting System 2.0 in Companies. Aptisi Transactions On Management.

1(2). pp.124-129.

Online

Difference Between Income Statement & Balance Sheets. 2019. [Online]. Available through:

<https://smallbusiness.chron.com/difference-between-income-statement-balance-sheets-

55419.html>.

Features of Financial Statements. 2019. [Online]. Available through:

<http://www.yourarticlelibrary.com/accounting/financial-statements/financial-statements-

features-importance-and-limitations/61727>.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.