Management Accounting Report: Performance, Costing and Budgeting

VerifiedAdded on 2021/01/01

|19

|4263

|481

Report

AI Summary

This report comprehensively analyzes management accounting principles, encompassing key areas such as costing methods, budgeting, and financial reporting. It begins with an introduction to management accounting, differentiating it from financial accounting and highlighting its importance for departmental decision-making. The report then delves into cost accounting systems, including actual, normal, and standard costing, along with inventory and job costing systems. Further, it examines the presentation of financial information, including various managerial accounting reports like budgeting, job cost, and performance reports, emphasizing the importance of implementing these reporting systems. The report also includes a comparative analysis of absorption and marginal costing methods, and explores the significance of budgeting as a tool for planning and control. The analysis provides insights into how these tools and techniques can improve business efficiency and support decision-making processes within an organization.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(A): Management Accounting and the essential requirements of management accounting

system.....................................................................................................................................1

(I): Distinguish in between management and financial accounting.......................................2

(II): The importance of management accounting information as a decision making tool for

department mangers................................................................................................................2

(III): Cost accounting systems:...............................................................................................3

(IV): Inventory management system......................................................................................3

(V): Job costing system:.........................................................................................................4

P2............................................................................................................................................4

b). Presenting financial information:......................................................................................4

II. Importance of implementing these reporting systems:......................................................5

M1...........................................................................................................................................5

D1...........................................................................................................................................5

TASK 2............................................................................................................................................6

P3 Calculation of net profits as per absorption costing and marginal costing:......................6

(I): Absorption Costing: .......................................................................................................6

(II): Marginal costing method:...............................................................................................8

M1...........................................................................................................................................9

D1...........................................................................................................................................9

TASK 3............................................................................................................................................9

a). Budgets and its advantages and disadvantages:................................................................9

(B):........................................................................................................................................11

(c): Importance of the budget as a tool for planning and control purpose:..........................11

M3.........................................................................................................................................11

D3.........................................................................................................................................12

TASK 4..........................................................................................................................................12

P5..........................................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(A): Management Accounting and the essential requirements of management accounting

system.....................................................................................................................................1

(I): Distinguish in between management and financial accounting.......................................2

(II): The importance of management accounting information as a decision making tool for

department mangers................................................................................................................2

(III): Cost accounting systems:...............................................................................................3

(IV): Inventory management system......................................................................................3

(V): Job costing system:.........................................................................................................4

P2............................................................................................................................................4

b). Presenting financial information:......................................................................................4

II. Importance of implementing these reporting systems:......................................................5

M1...........................................................................................................................................5

D1...........................................................................................................................................5

TASK 2............................................................................................................................................6

P3 Calculation of net profits as per absorption costing and marginal costing:......................6

(I): Absorption Costing: .......................................................................................................6

(II): Marginal costing method:...............................................................................................8

M1...........................................................................................................................................9

D1...........................................................................................................................................9

TASK 3............................................................................................................................................9

a). Budgets and its advantages and disadvantages:................................................................9

(B):........................................................................................................................................11

(c): Importance of the budget as a tool for planning and control purpose:..........................11

M3.........................................................................................................................................11

D3.........................................................................................................................................12

TASK 4..........................................................................................................................................12

P5..........................................................................................................................................12

M4.........................................................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

This is the device which is utilized amid the business activities with the goal that

principal of the referred to organization could bring down the expenses by evacuating an

additional cost. In spite of the fact that, this is rightly observed that the organization is

unequivocally prescribed to work together activities in a viable way. notwithstanding, this can be

said that there are such a large number of vital viewpoints those are shaping firm in an

exceedingly gainful way. Despite the fact that, this can be said that by executing a successful

management accounting systems for enhancing the execution of the firm. This would at last help

with dispensing with consumption of association. Those brought about amid creation of time.

Upgrading income and frame business choices for creating powerful comprehension of

bookkeeping instruments.

TASK 1

(A): Management Accounting and the essential requirements of management accounting system

Management accounting is utilization of statistical tools and techniques to producing and

illustrating the information in well- defined manner, which assists the management in its

functioning of increasing the efficiency and in envisaging, preparing and maintain the plans for

future and subsequently in calculating their execution. (Association of certified and corporate

accountants)

In managerial or management accounting, accounting information after analysing and

interpreting by objectives is presented to the management so as to help in the execution of

determination of policies, planning, decision making and coordinating functions (Abdel-Kader,

2011).

The essential requirements of management accounting system:

1 . It assists the company to evaluate the performance of each department by comparing the

actual performance with the planned performance.

2 It also helps in allocating the resources to various departments and utilizes the resources

by the departments in most appropriate manner.

3 The management accounting provides accounting information to the management which

helps them to prepare the financial statements of the company.

PAGE 14

This is the device which is utilized amid the business activities with the goal that

principal of the referred to organization could bring down the expenses by evacuating an

additional cost. In spite of the fact that, this is rightly observed that the organization is

unequivocally prescribed to work together activities in a viable way. notwithstanding, this can be

said that there are such a large number of vital viewpoints those are shaping firm in an

exceedingly gainful way. Despite the fact that, this can be said that by executing a successful

management accounting systems for enhancing the execution of the firm. This would at last help

with dispensing with consumption of association. Those brought about amid creation of time.

Upgrading income and frame business choices for creating powerful comprehension of

bookkeeping instruments.

TASK 1

(A): Management Accounting and the essential requirements of management accounting system

Management accounting is utilization of statistical tools and techniques to producing and

illustrating the information in well- defined manner, which assists the management in its

functioning of increasing the efficiency and in envisaging, preparing and maintain the plans for

future and subsequently in calculating their execution. (Association of certified and corporate

accountants)

In managerial or management accounting, accounting information after analysing and

interpreting by objectives is presented to the management so as to help in the execution of

determination of policies, planning, decision making and coordinating functions (Abdel-Kader,

2011).

The essential requirements of management accounting system:

1 . It assists the company to evaluate the performance of each department by comparing the

actual performance with the planned performance.

2 It also helps in allocating the resources to various departments and utilizes the resources

by the departments in most appropriate manner.

3 The management accounting provides accounting information to the management which

helps them to prepare the financial statements of the company.

PAGE 14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4 It also reduces the wastages and measures the external risk to the company.

5 While using the management accounting the manager prepare the plans and control them

by using their tools and techniques.

(I) Distinguish in between management and financial accounting

User of accounting: The users of the management accounting are mainly the managers

and departments employees whereas the users of the financial accounting are external which

includes stakeholders.

Transaction conducted by both the accounting: The management accounting focuses on

the non-monetary and monetary transaction whereas the financial accounting focuses on the

monetary transactions only.

Set of rules: The standards are not fixed for the management accounting they can prepare

their information in any manner according to their company’s management needs whereas the

standards are fixed for the financial accounting which should be followed by the organization.

Nature of information: The management accounting uses information is mainly related to

the past, present, and future oriented whereas the financial accounting uses information which is

past performance of the company (Callahan, Stetz and Brooks, 2011).

(II): Following are the importance of management accounting information as a decision making

tool for department mangers

Management accounting helps the manager while preparing plans for each department so

that each department can achieve their assigned targets on the prescribed time.

It also helps the manager of the company in buying or making decision related to the

product while considering the relevant factors.

The manager can use the important tools and techniques while preparing the strategies for

the company growth.

The manager also uses the management accounting information to assess the different

risk to the business activities and manage it in proper way.

With the help of management accounting information, the managers take the corrective

action to reduces and eliminate the deviation in the working processes.

PAGE 14

5 While using the management accounting the manager prepare the plans and control them

by using their tools and techniques.

(I) Distinguish in between management and financial accounting

User of accounting: The users of the management accounting are mainly the managers

and departments employees whereas the users of the financial accounting are external which

includes stakeholders.

Transaction conducted by both the accounting: The management accounting focuses on

the non-monetary and monetary transaction whereas the financial accounting focuses on the

monetary transactions only.

Set of rules: The standards are not fixed for the management accounting they can prepare

their information in any manner according to their company’s management needs whereas the

standards are fixed for the financial accounting which should be followed by the organization.

Nature of information: The management accounting uses information is mainly related to

the past, present, and future oriented whereas the financial accounting uses information which is

past performance of the company (Callahan, Stetz and Brooks, 2011).

(II): Following are the importance of management accounting information as a decision making

tool for department mangers

Management accounting helps the manager while preparing plans for each department so

that each department can achieve their assigned targets on the prescribed time.

It also helps the manager of the company in buying or making decision related to the

product while considering the relevant factors.

The manager can use the important tools and techniques while preparing the strategies for

the company growth.

The manager also uses the management accounting information to assess the different

risk to the business activities and manage it in proper way.

With the help of management accounting information, the managers take the corrective

action to reduces and eliminate the deviation in the working processes.

PAGE 14

l (III): Cost accounting systems:

This system gives the various tools and techniques to the manager to estimate the cost of

the product. It also helps the management to set the selling price of the product and they also

decide which expenses to be involve it or not. It includes measuring and reporting the product

costs. It system is basically used by the company to reduces their operating costs and wastage in

the system. The manufacturing activities of the company depend upon this system.

Various types of costing system are:

Actual costing system: The actual costing system is used to record the costs of the

product which are based on actual cost of raw material, labour, and overhead aroused on the

goods which are apportioned on the ground of the actual quantity of the apportion basis seen

during the reporting time. The actual costing is the easy costing system which does not need any

pre- determined of the budgeted cost.

Normal costing system: Normal costing system utilized of the estimated amount of

overhead for the measurement of the product cost. It uses the estimated overhead rate which

ensures the measurement of cost where the suddenly rises in the cost which is not expected.

Standard costing system: The standard costing is the costing, where the forecasted cost is

changed by the actual cost in the records of accounting and then the differences are identified

periodically that represents the variances between the expected and actual cost. This system

assists in measurement and evaluation of the performance of the department (Hopper and Bui,

2016).

l (IV): Inventory management system

This system keeps track the inventory in the whole manufacturing process of the product.

The production processes in TECH (UK) LTD. can be consolidated with the inventory

system to achieve the effectual and accurate inventory flow within the production system of the

company.

This system gives information to the manager about the current status of the inventory, in

how much time the next order can be placed by the company, supplier status, etc.

This system assists the company in prior planning and controlling of the purchasing cost

of an inventory and carrying cost of the inventory and how to reduce the dead stock in the

system.

PAGE 14

This system gives the various tools and techniques to the manager to estimate the cost of

the product. It also helps the management to set the selling price of the product and they also

decide which expenses to be involve it or not. It includes measuring and reporting the product

costs. It system is basically used by the company to reduces their operating costs and wastage in

the system. The manufacturing activities of the company depend upon this system.

Various types of costing system are:

Actual costing system: The actual costing system is used to record the costs of the

product which are based on actual cost of raw material, labour, and overhead aroused on the

goods which are apportioned on the ground of the actual quantity of the apportion basis seen

during the reporting time. The actual costing is the easy costing system which does not need any

pre- determined of the budgeted cost.

Normal costing system: Normal costing system utilized of the estimated amount of

overhead for the measurement of the product cost. It uses the estimated overhead rate which

ensures the measurement of cost where the suddenly rises in the cost which is not expected.

Standard costing system: The standard costing is the costing, where the forecasted cost is

changed by the actual cost in the records of accounting and then the differences are identified

periodically that represents the variances between the expected and actual cost. This system

assists in measurement and evaluation of the performance of the department (Hopper and Bui,

2016).

l (IV): Inventory management system

This system keeps track the inventory in the whole manufacturing process of the product.

The production processes in TECH (UK) LTD. can be consolidated with the inventory

system to achieve the effectual and accurate inventory flow within the production system of the

company.

This system gives information to the manager about the current status of the inventory, in

how much time the next order can be placed by the company, supplier status, etc.

This system assists the company in prior planning and controlling of the purchasing cost

of an inventory and carrying cost of the inventory and how to reduce the dead stock in the

system.

PAGE 14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(V) Job costing system:

A job costing system is a system of recording the cost and then accumulates it. The specific

activity (job or group of tasks) are collected which is shown on job card.

The function of job costing system:

Helps in planning, control of cost and decision making by establishing cost (costs are

recorded on job cards), measuring the sales price, finding profit/ loss on jobs.

The job costing system easily traced all stages of production within the factory.

TECH (UK) LTD. can use this system when they produce the product on the basis of

customer specifications and order is of comparatively short duration (Leitner, 2013).

P2

b). Presenting financial information:

I. Different types managerial accounting reports:

1 Budgeting reports: The Budgetary reports lay out the plan to examine the department’s

performance according to the pre decided by the manager. For the preparation of the budget

reports the actual expenditure incurred in the past get utilized by the manager. This report helps

the manager to prepare the budget for the future so that the company achieves their target on the

time.

2 Job cost reports: The job cost reports record all the transaction related to the specific

product which the company manufactured on the basis of customer specification. It records all

the cost, expenses and profit margin of all specified job in this report. This report helps the

customer to measure the cost of specified product and accordingly they placed an order to the

company. This report assists the company to reduce the wastage of the time on the project which

is in progress and also evaluate and maintain the cost of the project.

3 Performance reports: The performance reports show the overall performance of the

company in all aspects. The differences are calculated by comparing the estimated performance

with the actual results and denoted in this report. The performance reports help the investor to

measures the achievement of the company and accordingly they invest their money in the

company’s project. With the help of this report the company can take the loan from the financial

institutions for their projects. This reports are prepared annually depends upon the company

policies (Nielsen, Mitchell and Nørreklit, 2015).

PAGE 14

A job costing system is a system of recording the cost and then accumulates it. The specific

activity (job or group of tasks) are collected which is shown on job card.

The function of job costing system:

Helps in planning, control of cost and decision making by establishing cost (costs are

recorded on job cards), measuring the sales price, finding profit/ loss on jobs.

The job costing system easily traced all stages of production within the factory.

TECH (UK) LTD. can use this system when they produce the product on the basis of

customer specifications and order is of comparatively short duration (Leitner, 2013).

P2

b). Presenting financial information:

I. Different types managerial accounting reports:

1 Budgeting reports: The Budgetary reports lay out the plan to examine the department’s

performance according to the pre decided by the manager. For the preparation of the budget

reports the actual expenditure incurred in the past get utilized by the manager. This report helps

the manager to prepare the budget for the future so that the company achieves their target on the

time.

2 Job cost reports: The job cost reports record all the transaction related to the specific

product which the company manufactured on the basis of customer specification. It records all

the cost, expenses and profit margin of all specified job in this report. This report helps the

customer to measure the cost of specified product and accordingly they placed an order to the

company. This report assists the company to reduce the wastage of the time on the project which

is in progress and also evaluate and maintain the cost of the project.

3 Performance reports: The performance reports show the overall performance of the

company in all aspects. The differences are calculated by comparing the estimated performance

with the actual results and denoted in this report. The performance reports help the investor to

measures the achievement of the company and accordingly they invest their money in the

company’s project. With the help of this report the company can take the loan from the financial

institutions for their projects. This reports are prepared annually depends upon the company

policies (Nielsen, Mitchell and Nørreklit, 2015).

PAGE 14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4 Situation or opportunity reports: These reports are basically maintained by the

management of the company so that everyone in the organization can be attentive of the

happening of the specific event. The well-structured report assists the management to take the

decision for the company’s business while considering the events which have adverse and

favourable impact on the business.

l II. Importance of implementing these reporting systems:

It is very essential that the management accounting information to be represented in

manner that must be clear to each and every department of the company. This information helps

the department to set out their targets and accordingly they achieved it in estimated time fix by

the management. This information helps the management to prepare the strategies for the future.

Well-defined information produced by the top management for whole organization should be in

understandable format. TECH (UK) LTD. integrates the organizational processes with the

management information system where they stored the information and user can use this

information for their needs and also stored to this system.

l M1

The management accounting system help the TECH (UK) LTD. in the finding the cost

throughout the production process. By using the cost accounting system the manager of the

company can evaluate the business efficiency and also improves efficiency in processes when it

is requires. By applying management accounting system tools and techniques the TECH (UK)

LTD. improve the accuracy in its inventory system and also saves the time and avoid

unnecessary wastages in the business activities. The management accounting system is also

assists the management to maximize their operating profits by maintaining the cost of the

product. TECH (UK) LTD. can use the effective and useful management accounting system for

their business activities and also for preparing the policies and strategies for their concern.

l D1

The effective management accounting system assists the management of the TECH (UK)

LTD. to make the reports for their departments and also for entire organization. Both the

management accounting reporting and system integrates with the organizational processes of the

TECH (UK) LTD. helps to prepare the plans for their business activities. Effective reporting

system helps the company to achieve their targets which are prescribed for the future goals. The

PAGE 14

management of the company so that everyone in the organization can be attentive of the

happening of the specific event. The well-structured report assists the management to take the

decision for the company’s business while considering the events which have adverse and

favourable impact on the business.

l II. Importance of implementing these reporting systems:

It is very essential that the management accounting information to be represented in

manner that must be clear to each and every department of the company. This information helps

the department to set out their targets and accordingly they achieved it in estimated time fix by

the management. This information helps the management to prepare the strategies for the future.

Well-defined information produced by the top management for whole organization should be in

understandable format. TECH (UK) LTD. integrates the organizational processes with the

management information system where they stored the information and user can use this

information for their needs and also stored to this system.

l M1

The management accounting system help the TECH (UK) LTD. in the finding the cost

throughout the production process. By using the cost accounting system the manager of the

company can evaluate the business efficiency and also improves efficiency in processes when it

is requires. By applying management accounting system tools and techniques the TECH (UK)

LTD. improve the accuracy in its inventory system and also saves the time and avoid

unnecessary wastages in the business activities. The management accounting system is also

assists the management to maximize their operating profits by maintaining the cost of the

product. TECH (UK) LTD. can use the effective and useful management accounting system for

their business activities and also for preparing the policies and strategies for their concern.

l D1

The effective management accounting system assists the management of the TECH (UK)

LTD. to make the reports for their departments and also for entire organization. Both the

management accounting reporting and system integrates with the organizational processes of the

TECH (UK) LTD. helps to prepare the plans for their business activities. Effective reporting

system helps the company to achieve their targets which are prescribed for the future goals. The

PAGE 14

reporting system helps the management in all aspects like in inventory, job, performance,

receivables etc.

TASK 2

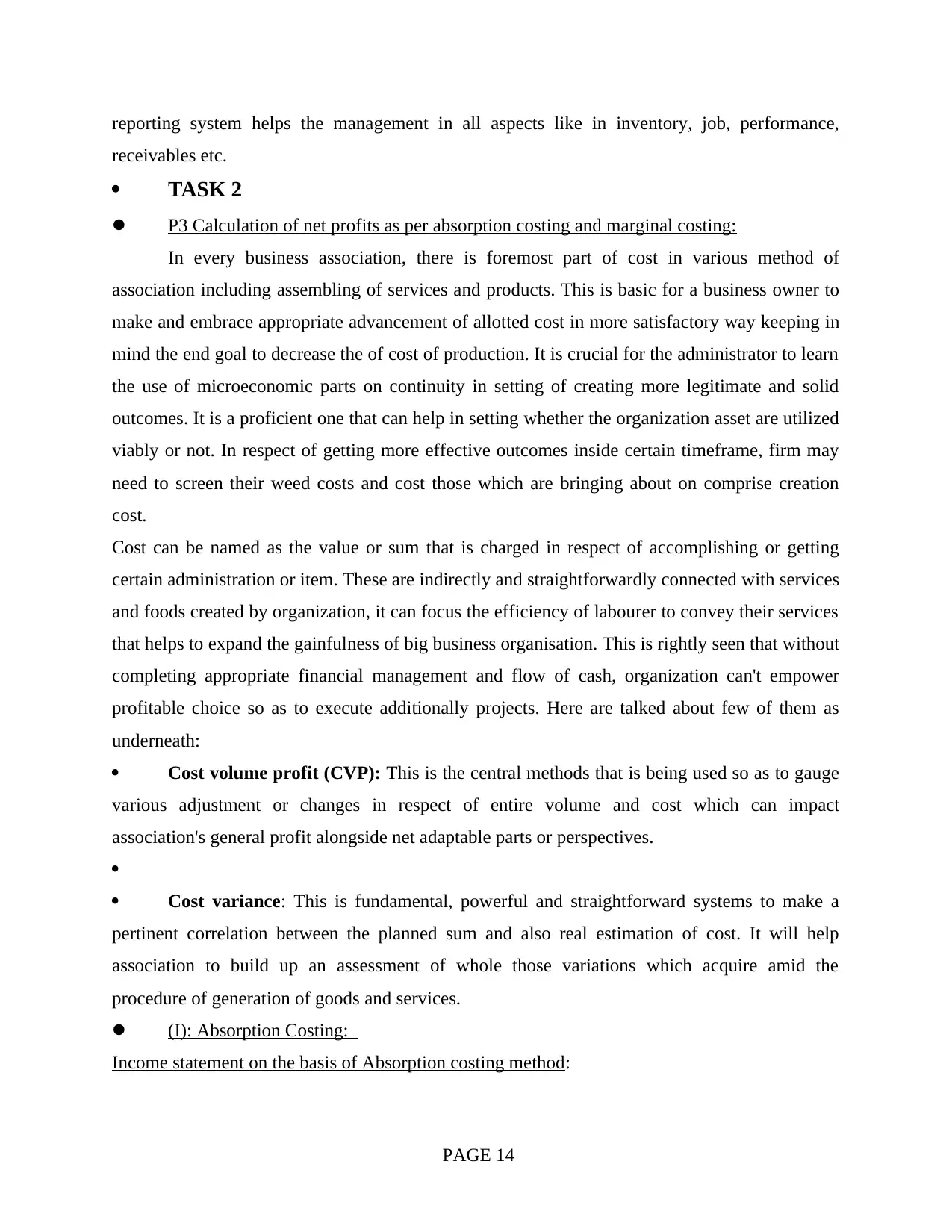

l P3 Calculation of net profits as per absorption costing and marginal costing:

In every business association, there is foremost part of cost in various method of

association including assembling of services and products. This is basic for a business owner to

make and embrace appropriate advancement of allotted cost in more satisfactory way keeping in

mind the end goal to decrease the of cost of production. It is crucial for the administrator to learn

the use of microeconomic parts on continuity in setting of creating more legitimate and solid

outcomes. It is a proficient one that can help in setting whether the organization asset are utilized

viably or not. In respect of getting more effective outcomes inside certain timeframe, firm may

need to screen their weed costs and cost those which are bringing about on comprise creation

cost.

Cost can be named as the value or sum that is charged in respect of accomplishing or getting

certain administration or item. These are indirectly and straightforwardly connected with services

and foods created by organization, it can focus the efficiency of labourer to convey their services

that helps to expand the gainfulness of big business organisation. This is rightly seen that without

completing appropriate financial management and flow of cash, organization can't empower

profitable choice so as to execute additionally projects. Here are talked about few of them as

underneath:

Cost volume profit (CVP): This is the central methods that is being used so as to gauge

various adjustment or changes in respect of entire volume and cost which can impact

association's general profit alongside net adaptable parts or perspectives.

Cost variance: This is fundamental, powerful and straightforward systems to make a

pertinent correlation between the planned sum and also real estimation of cost. It will help

association to build up an assessment of whole those variations which acquire amid the

procedure of generation of goods and services.

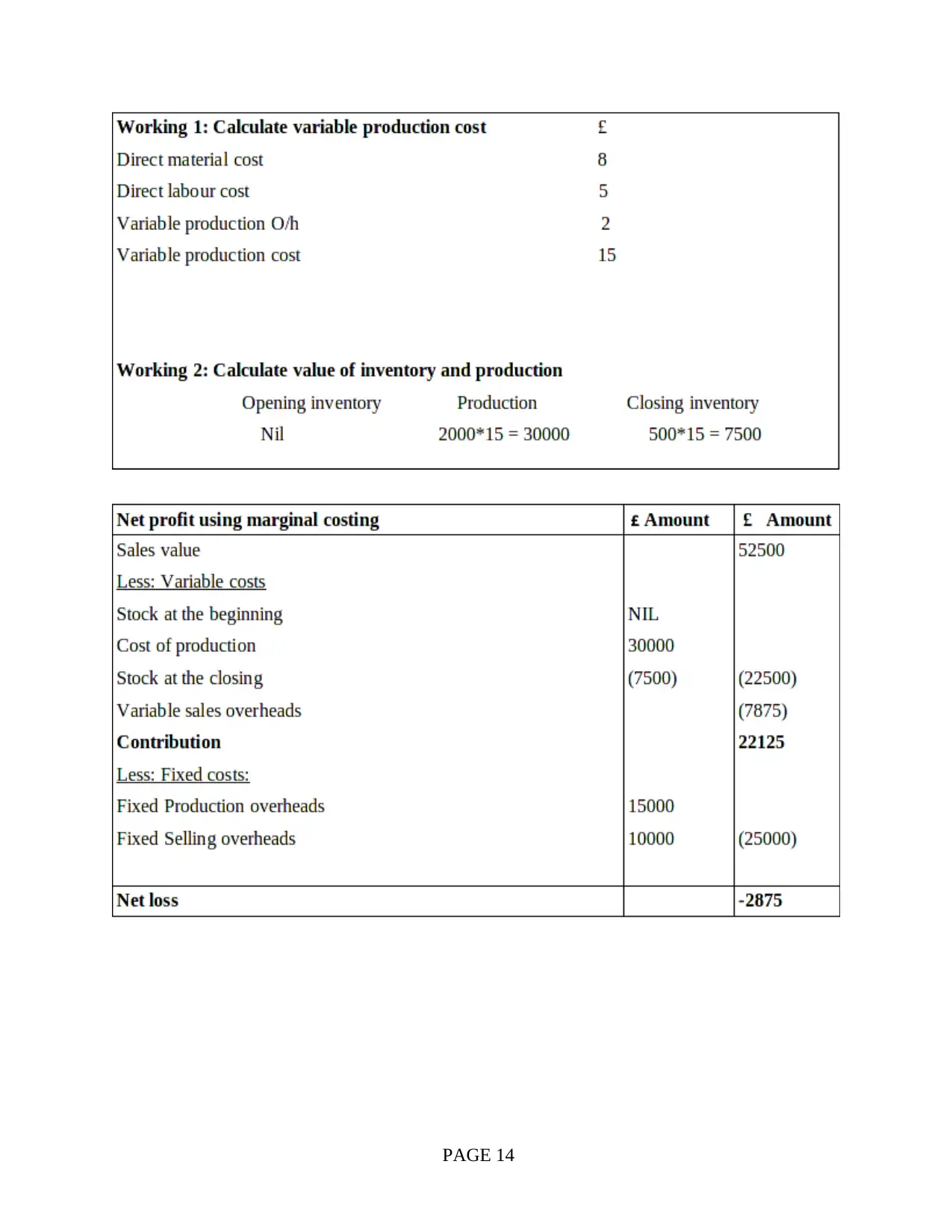

l (I): Absorption Costing:

Income statement on the basis of Absorption costing method:

PAGE 14

receivables etc.

TASK 2

l P3 Calculation of net profits as per absorption costing and marginal costing:

In every business association, there is foremost part of cost in various method of

association including assembling of services and products. This is basic for a business owner to

make and embrace appropriate advancement of allotted cost in more satisfactory way keeping in

mind the end goal to decrease the of cost of production. It is crucial for the administrator to learn

the use of microeconomic parts on continuity in setting of creating more legitimate and solid

outcomes. It is a proficient one that can help in setting whether the organization asset are utilized

viably or not. In respect of getting more effective outcomes inside certain timeframe, firm may

need to screen their weed costs and cost those which are bringing about on comprise creation

cost.

Cost can be named as the value or sum that is charged in respect of accomplishing or getting

certain administration or item. These are indirectly and straightforwardly connected with services

and foods created by organization, it can focus the efficiency of labourer to convey their services

that helps to expand the gainfulness of big business organisation. This is rightly seen that without

completing appropriate financial management and flow of cash, organization can't empower

profitable choice so as to execute additionally projects. Here are talked about few of them as

underneath:

Cost volume profit (CVP): This is the central methods that is being used so as to gauge

various adjustment or changes in respect of entire volume and cost which can impact

association's general profit alongside net adaptable parts or perspectives.

Cost variance: This is fundamental, powerful and straightforward systems to make a

pertinent correlation between the planned sum and also real estimation of cost. It will help

association to build up an assessment of whole those variations which acquire amid the

procedure of generation of goods and services.

l (I): Absorption Costing:

Income statement on the basis of Absorption costing method:

PAGE 14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PAGE 14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

PAGE 14

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

PAGE 14

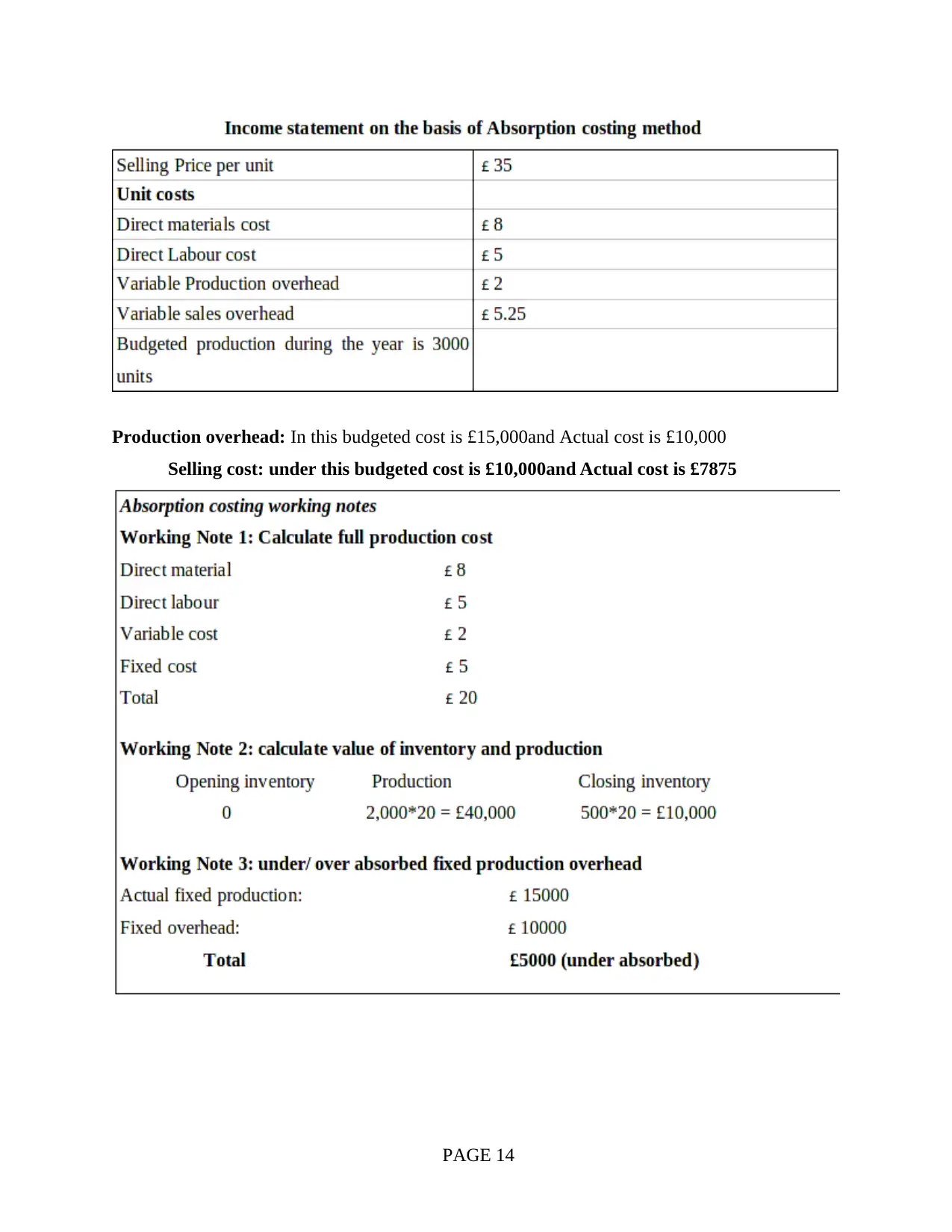

l M1

Here are various kinds of techniques which are required to be used by the organisation

for measuring net profits in properly way. However, various kinds of methods can be used by the

company for optimising the profits in an effective manner. Cost volume profits analysis,

absorption costing, and marginal costing methods and so on that can be utilized by the cited

company for optimising the profits in an effectual manner.

l D1

Absorption costing and marginal costing methods are used by the organisation for calculating the

net profits. Although, this can be concluded that the management of the Tech (UK) use the

absorption costing method to measure the net operating profits. Here, the net operating loss as

per the marginal costing is -2875 while, net operating profits as per the absorption costing is

calculated which is also in the loss but better than the loss calculated as per the marginal costing.

As there is only is -375.

PAGE 14

Here are various kinds of techniques which are required to be used by the organisation

for measuring net profits in properly way. However, various kinds of methods can be used by the

company for optimising the profits in an effective manner. Cost volume profits analysis,

absorption costing, and marginal costing methods and so on that can be utilized by the cited

company for optimising the profits in an effectual manner.

l D1

Absorption costing and marginal costing methods are used by the organisation for calculating the

net profits. Although, this can be concluded that the management of the Tech (UK) use the

absorption costing method to measure the net operating profits. Here, the net operating loss as

per the marginal costing is -2875 while, net operating profits as per the absorption costing is

calculated which is also in the loss but better than the loss calculated as per the marginal costing.

As there is only is -375.

PAGE 14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.