Taxation Assignment: Deductible Expenses, GST, and Offset Calculations

VerifiedAdded on 2020/03/01

|11

|2895

|34

Homework Assignment

AI Summary

This assignment provides a detailed analysis of taxation principles, focusing on deductible expenses under section 8-1 of the ITAA 1997, GST implications for businesses like Big Bank Ltd, and foreign tax offsets. The first part examines the allowability of various expenses, such as the cost of moving machinery, asset revaluation, and legal expenses, providing insights into their treatment for tax purposes. The second part delves into GST, specifically addressing the eligibility of Big Bank Ltd to claim input tax credit on advertising expenditures and the relevant conditions. The final part covers foreign tax offsets, illustrating the computation of assessable income and the application of foreign tax credits with examples. The assignment covers topics like employment, rental, dividend, and interest income from multiple countries.

TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

Answer to 1

According to section 8-1 of the ITAA 1997, deductible expenses are the one that is incurred

either while earning the assessable income or while functioning a business that can assist in the

attainment of such assessable income. Further, deduction of these expenses is not allowable as a

deduction that is private or capital in nature, or the expenses that are in association with the

attainment of exempted income.

i. In the case of cost of moving machinery to a new place, the same is related to brand

new machinery that is deported from the area of purchase to the site. Moreover, the

expense incurred here must be incorporated in the Machinery's capital cost and

therefore, it is deemed to be of capital nature. Therefore, such expenses must not be

allowable under the above-mentioned section 8-1 because they are of capital origin

and the given section does not allow such expenses. Further, adding up to such

expenses or allowability of expenses rely upon an asset’s nature whether it is an old

one or brand-new (Fullerton et. al, 2017). If the asset is brand new in nature, every

expense that is incurred up to the date of its utilization must be summed up to its cost

and it must become a part of the asset’s cost. For instance, commissioning,

installation, and transportation cost, etc. Besides, in the case wherein the expense is

incurred for deporting the old machine from the present location to a new location, it

must be deemed to be regarded as transportation cost and therefore, allowable as

deduction.

ii. In the case of revaluation of assets to effect insurance cover, it can be seen that the

expenses incurred for the assets’ evaluation in order to claim exemption are allowable

only if they are incurred for recovery of loss of gain, whether directly or indirectly

related to the assessable income. Besides, in relation to an insurance claim, two

scenarios can arise. Firstly, in relation to an asset for which insurance claim is

attained is of capital nature, this implies that the capital asset is wrecked and the claim

is mainly for the recovery of losses. Nevertheless, in such a scenario, the incurred

expenses for the recovery of insurance coverage must be subtracted from the original

insurance claim amount and the same must not be regarded as business expenditure.

Secondly, when the insurance claim is for attaining loss on assets that are directly

2

Answer to 1

According to section 8-1 of the ITAA 1997, deductible expenses are the one that is incurred

either while earning the assessable income or while functioning a business that can assist in the

attainment of such assessable income. Further, deduction of these expenses is not allowable as a

deduction that is private or capital in nature, or the expenses that are in association with the

attainment of exempted income.

i. In the case of cost of moving machinery to a new place, the same is related to brand

new machinery that is deported from the area of purchase to the site. Moreover, the

expense incurred here must be incorporated in the Machinery's capital cost and

therefore, it is deemed to be of capital nature. Therefore, such expenses must not be

allowable under the above-mentioned section 8-1 because they are of capital origin

and the given section does not allow such expenses. Further, adding up to such

expenses or allowability of expenses rely upon an asset’s nature whether it is an old

one or brand-new (Fullerton et. al, 2017). If the asset is brand new in nature, every

expense that is incurred up to the date of its utilization must be summed up to its cost

and it must become a part of the asset’s cost. For instance, commissioning,

installation, and transportation cost, etc. Besides, in the case wherein the expense is

incurred for deporting the old machine from the present location to a new location, it

must be deemed to be regarded as transportation cost and therefore, allowable as

deduction.

ii. In the case of revaluation of assets to effect insurance cover, it can be seen that the

expenses incurred for the assets’ evaluation in order to claim exemption are allowable

only if they are incurred for recovery of loss of gain, whether directly or indirectly

related to the assessable income. Besides, in relation to an insurance claim, two

scenarios can arise. Firstly, in relation to an asset for which insurance claim is

attained is of capital nature, this implies that the capital asset is wrecked and the claim

is mainly for the recovery of losses. Nevertheless, in such a scenario, the incurred

expenses for the recovery of insurance coverage must be subtracted from the original

insurance claim amount and the same must not be regarded as business expenditure.

Secondly, when the insurance claim is for attaining loss on assets that are directly

2

Taxation

held as stock in trade, such assets cannot be regarded as capital assets and is therefore

directly associated with the assessable income being depicted in the financials.

Further, any incurred expenses for such purpose are allowable only as business

expenditures so that businesses can attain benefit from the same. Nevertheless, these

expenses must be shown in the profit and loss account and considered as expenses for

recovering the losses on the stock. On a whole, the expenses incurred for revaluation

of assets held as stock in trade can be allowed under 8-1 of the ITAA, 1997.

iii. As mentioned previously, under section 8-1 of the ITAA, 1997, it has been stated that

deductible expenses are either incurred while earning the assessable income or while

operating a particular business that plays the main role in generating such assessable

income. Furthermore, the deduction is not allowable of these expenses if they are of

domestic nature, capital nature, or nature in association with the attainment of

exempted income. A similar instance was held in the case of Newspapers Ltd v

FCT(1938) 61 CLR 337) where all losses and payments that include commission,

expenses of traveling, expenses and not in the nature of losses and capital outgoing

provided in gaining the income that is assessable. Therefore, in computing the

taxpayer taxable income, the overall income generated by the taxpayer shall be

considered.

Therefore, in the given situation, if such ideology is implemented, it can be stated that

the legal expenses that the company has incurred for tackling a petition for winding

up cannot fall under the purview of the said section. This is because it is not incurred

for earning an assessable income and it is not the expenses that are incurred

compulsorily to operate the business so that assessable income can be attained.

Furthermore, the paid expenses must also be verified in the light of the net amount

because bigger the figure, the more impossible it will be to treat such as business

expenses. However, since it is a legal expenditure that has been incurred for the

purpose of carrying on the business operation, it can be regarded as an expense that is

allowable under section 25-5.

iv. It can be observed in the given case that the solicitor account does not segregate the

expenses in relation to several matters and therefore, many legal expenses fail to be

divided into revenue or capital nature. Further, it has been assumed that the legal

3

held as stock in trade, such assets cannot be regarded as capital assets and is therefore

directly associated with the assessable income being depicted in the financials.

Further, any incurred expenses for such purpose are allowable only as business

expenditures so that businesses can attain benefit from the same. Nevertheless, these

expenses must be shown in the profit and loss account and considered as expenses for

recovering the losses on the stock. On a whole, the expenses incurred for revaluation

of assets held as stock in trade can be allowed under 8-1 of the ITAA, 1997.

iii. As mentioned previously, under section 8-1 of the ITAA, 1997, it has been stated that

deductible expenses are either incurred while earning the assessable income or while

operating a particular business that plays the main role in generating such assessable

income. Furthermore, the deduction is not allowable of these expenses if they are of

domestic nature, capital nature, or nature in association with the attainment of

exempted income. A similar instance was held in the case of Newspapers Ltd v

FCT(1938) 61 CLR 337) where all losses and payments that include commission,

expenses of traveling, expenses and not in the nature of losses and capital outgoing

provided in gaining the income that is assessable. Therefore, in computing the

taxpayer taxable income, the overall income generated by the taxpayer shall be

considered.

Therefore, in the given situation, if such ideology is implemented, it can be stated that

the legal expenses that the company has incurred for tackling a petition for winding

up cannot fall under the purview of the said section. This is because it is not incurred

for earning an assessable income and it is not the expenses that are incurred

compulsorily to operate the business so that assessable income can be attained.

Furthermore, the paid expenses must also be verified in the light of the net amount

because bigger the figure, the more impossible it will be to treat such as business

expenses. However, since it is a legal expenditure that has been incurred for the

purpose of carrying on the business operation, it can be regarded as an expense that is

allowable under section 25-5.

iv. It can be observed in the given case that the solicitor account does not segregate the

expenses in relation to several matters and therefore, many legal expenses fail to be

divided into revenue or capital nature. Further, it has been assumed that the legal

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

expenses for each affair mentioned in the situation are incurred for the purpose of the

business itself. In addition, such expenses have been incurred for the purpose of

income recovery that must further become a relevant part of the assessable income

(Kobestky, 2005). Therefore, if the purposes are segregated, it can be stated that the

legal expenses that have been incurred for the discharge of mortgage can be regarded

as an expense of capital nature and hence, the same cannot be allowed under section

8-1 of the ITAA 1997. Besides, all other incurred expenses can be easily allowable as

deduction.

Hence, it can be concluded why the previously mentioned expenses are either allowable or

disallowable in the businesses.

4

expenses for each affair mentioned in the situation are incurred for the purpose of the

business itself. In addition, such expenses have been incurred for the purpose of

income recovery that must further become a relevant part of the assessable income

(Kobestky, 2005). Therefore, if the purposes are segregated, it can be stated that the

legal expenses that have been incurred for the discharge of mortgage can be regarded

as an expense of capital nature and hence, the same cannot be allowed under section

8-1 of the ITAA 1997. Besides, all other incurred expenses can be easily allowable as

deduction.

Hence, it can be concluded why the previously mentioned expenses are either allowable or

disallowable in the businesses.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

Answer to 2

It can be witnessed from the given scenario that Big Bank Ltd is a bank that is registered under

the GST scheme and functions on a national basis. This can be supported by the fact that it

possesses more than fifty branches and pursues a massive ten-story office and other innumerable

call centers for addressing its customers. Nevertheless, Big Bank has been offering various

facilities to its customers that include safety deposit and offering of loans. Besides, the bank has

also launched its product that is associated with contents and home insurance policies and it is

considered as one of the significant initiatives in its business. However, the bank must take

adequate steps to alter its computerized accounting system because of the prevalence of GST

scheme that must be charged on every premium policy offered by it to its customers (Kenny et.

al, 2016). Moreover, the bank is also under an obligation to advertise and promote such new

initiative because it has already made every effort to proceed with enhanced force in the

insurance industry. Such effort also includes preparation of appropriate budgeting strategies and

promotion through platforms like print media, television, etc that can enable in paving out ways

for an effective future. Big Bank has expended an amount of $16,50,000 for the advertising

campaign of such new initiative wherein $550,000 has been expended for promoting the newly

launched product and the remaining amount for other requirements. Moreover, the advertisement

consultant has also offered an invoice amounting to $16,50,000 for its services. The similar

instance has been observed in the case of House of Lords in C & E Commrs v Redrow Group plc

where the issue consisted in claiming of the input tax on the commissions charged to it by the

agent services.

In relation to this, the input tax credit of the same must be available to the Bank because it is a

registered user under the scheme of GST. The business of Big Bank must be allowed the tax

credit of the amount paid on the invoice (advertising bill) because it is usual business

expenditure and it is incurred especially for the purpose of business only (Martin, 2001).

Besides, such expense cannot be capitalized because it is not a one-time expense and it will recur

in future. Further, the life of such expense is short in nature and therefore, it must not be summed

up or regarded as the company’s asset (Pratt & Kulsrud, 2013).

Nevertheless, whenever any business entity expends for an expense that has been incurred for the

purpose of its business and such expense also accommodates GST scheme, then such entity has

5

Answer to 2

It can be witnessed from the given scenario that Big Bank Ltd is a bank that is registered under

the GST scheme and functions on a national basis. This can be supported by the fact that it

possesses more than fifty branches and pursues a massive ten-story office and other innumerable

call centers for addressing its customers. Nevertheless, Big Bank has been offering various

facilities to its customers that include safety deposit and offering of loans. Besides, the bank has

also launched its product that is associated with contents and home insurance policies and it is

considered as one of the significant initiatives in its business. However, the bank must take

adequate steps to alter its computerized accounting system because of the prevalence of GST

scheme that must be charged on every premium policy offered by it to its customers (Kenny et.

al, 2016). Moreover, the bank is also under an obligation to advertise and promote such new

initiative because it has already made every effort to proceed with enhanced force in the

insurance industry. Such effort also includes preparation of appropriate budgeting strategies and

promotion through platforms like print media, television, etc that can enable in paving out ways

for an effective future. Big Bank has expended an amount of $16,50,000 for the advertising

campaign of such new initiative wherein $550,000 has been expended for promoting the newly

launched product and the remaining amount for other requirements. Moreover, the advertisement

consultant has also offered an invoice amounting to $16,50,000 for its services. The similar

instance has been observed in the case of House of Lords in C & E Commrs v Redrow Group plc

where the issue consisted in claiming of the input tax on the commissions charged to it by the

agent services.

In relation to this, the input tax credit of the same must be available to the Bank because it is a

registered user under the scheme of GST. The business of Big Bank must be allowed the tax

credit of the amount paid on the invoice (advertising bill) because it is usual business

expenditure and it is incurred especially for the purpose of business only (Martin, 2001).

Besides, such expense cannot be capitalized because it is not a one-time expense and it will recur

in future. Further, the life of such expense is short in nature and therefore, it must not be summed

up or regarded as the company’s asset (Pratt & Kulsrud, 2013).

Nevertheless, whenever any business entity expends for an expense that has been incurred for the

purpose of its business and such expense also accommodates GST scheme, then such entity has

5

Taxation

the complete right to claim the credit for the amount of GST paid on the bill. This claiming of

credit on GST is also commonly known as GST or input tax credit.

As per Sadiq et. al (2017) claiming of GST can be allowed if the given below conditions comply:

a. The expenses that are incurred for any purchase of items are exclusively for the intention

of business and not for personal utilization.

b. GST must be incorporated in the purchase price of the item.

c. There must be a valid consideration for the payment of item purchased.

d. The seller or supplier of such item must issue a tax invoice for such item and it must be

inclusive of GST.

The expenses that are incurred by the Big Bank is an enormous figure but still, it must be

allowed as an advertising expenditure, as it is significantly or exclusively incurred for the

purpose of promoting the business operations of the bank. Further, the company also has

complete authority to claim the entire input tax credit so that it can be utilized for addressing its

additional tax liabilities of GST. A similar observation was noted in the case of Polysar

Investments Netherlands BV v Inspecteur der Invoerrechten en Accijnzen, Arnhem (Case C-

60/90). The question that was put before the court of justice was that whether Polysar can be

considered as a taxable entity for the purpose of VAT and whether input tax credit charged on

costs will be claimable. The court of justice came with a judgment that a holding company

having a primary purpose of holding shares in the subsidiary company and exercising rights with

the same will not be a taxable entity for the purpose of VAT and the status did not alter because

it is under the ambit of the economic grouping (Martin, 2001). Hence, it came to the conclusion

that input tax will not be available.

Moreover, the payment made by the bank to the advertisement consultants comprise of $550000

that is apportioned to the advertisement, television, and $11,00,000 for other advertising media.

Hence, such expense will assist the bank to enhance its business affairs and it must be

approximately two percent of its entire business affairs. Thus, the remaining 98% of the business

affairs of the bank must accrue to the traditional bank's sources of income that are deposit

facilities and distribution of loan to various customers, and for which commission and interest

are charged respectively (Renton, 2005). Therefore, since all these scenarios comply in the case

6

the complete right to claim the credit for the amount of GST paid on the bill. This claiming of

credit on GST is also commonly known as GST or input tax credit.

As per Sadiq et. al (2017) claiming of GST can be allowed if the given below conditions comply:

a. The expenses that are incurred for any purchase of items are exclusively for the intention

of business and not for personal utilization.

b. GST must be incorporated in the purchase price of the item.

c. There must be a valid consideration for the payment of item purchased.

d. The seller or supplier of such item must issue a tax invoice for such item and it must be

inclusive of GST.

The expenses that are incurred by the Big Bank is an enormous figure but still, it must be

allowed as an advertising expenditure, as it is significantly or exclusively incurred for the

purpose of promoting the business operations of the bank. Further, the company also has

complete authority to claim the entire input tax credit so that it can be utilized for addressing its

additional tax liabilities of GST. A similar observation was noted in the case of Polysar

Investments Netherlands BV v Inspecteur der Invoerrechten en Accijnzen, Arnhem (Case C-

60/90). The question that was put before the court of justice was that whether Polysar can be

considered as a taxable entity for the purpose of VAT and whether input tax credit charged on

costs will be claimable. The court of justice came with a judgment that a holding company

having a primary purpose of holding shares in the subsidiary company and exercising rights with

the same will not be a taxable entity for the purpose of VAT and the status did not alter because

it is under the ambit of the economic grouping (Martin, 2001). Hence, it came to the conclusion

that input tax will not be available.

Moreover, the payment made by the bank to the advertisement consultants comprise of $550000

that is apportioned to the advertisement, television, and $11,00,000 for other advertising media.

Hence, such expense will assist the bank to enhance its business affairs and it must be

approximately two percent of its entire business affairs. Thus, the remaining 98% of the business

affairs of the bank must accrue to the traditional bank's sources of income that are deposit

facilities and distribution of loan to various customers, and for which commission and interest

are charged respectively (Renton, 2005). Therefore, since all these scenarios comply in the case

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

of Big Bank Ltd, it is surely eligible to claim input tax credit on the invoice issued by the

advertising consultants (Hopewell, 2012).

Answer to 3

Whenever an individual attains income from a country wherein he is a usual resident and from

countries as well, then he has a right to go for the foreign offset of tax. Moreover, if such

individual has income from more than one country and he has incurred expenses for attaining

such income, he can offset such expenses only if the following conditions are satisfied:

a. Such individual has paid the foreign income tax from income generated from such

foreign country, which means that tax on such income has already been paid.

b. Such person has incorporated the foreign income in the net assessable income for

computing the total tax payable on income (Hopewell, 2012).

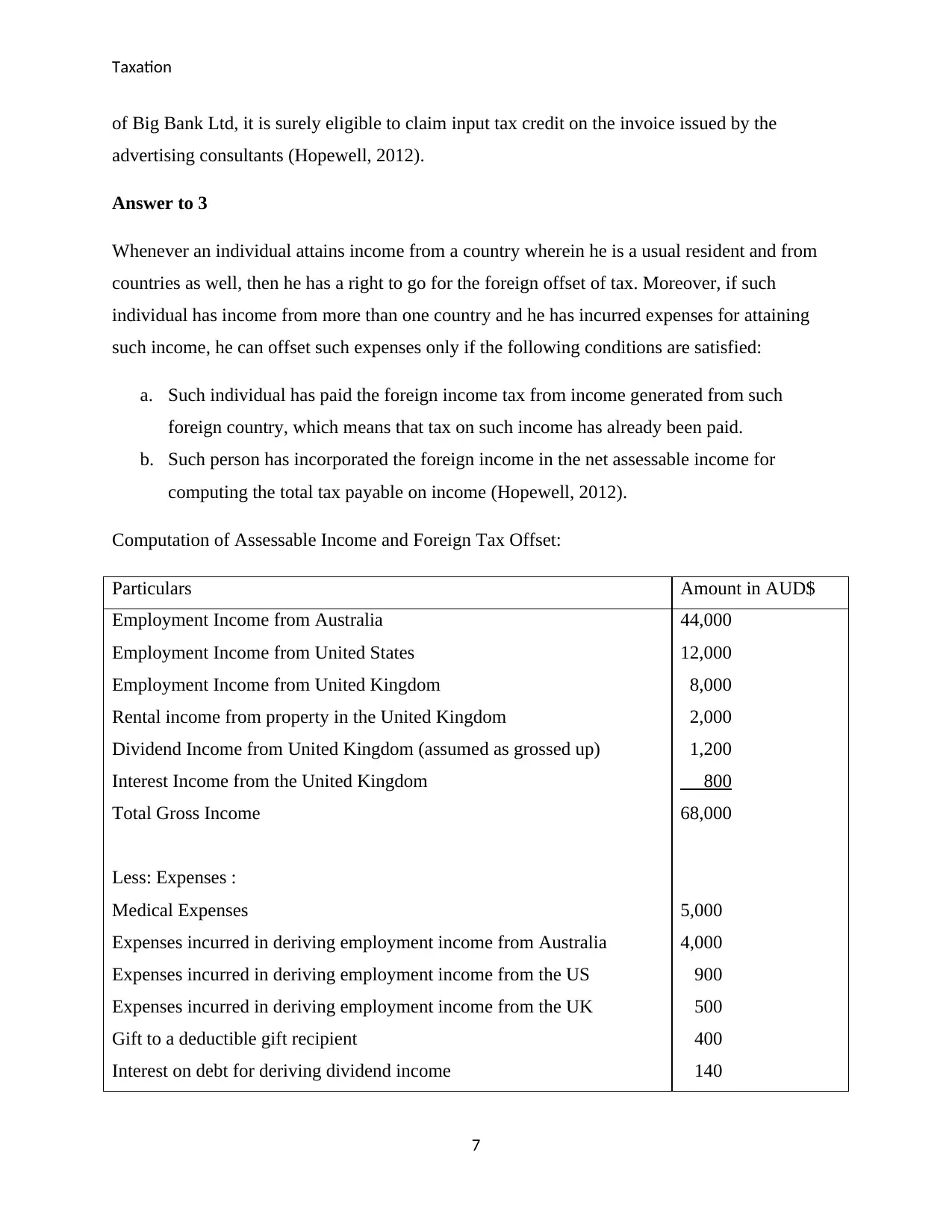

Computation of Assessable Income and Foreign Tax Offset:

Particulars Amount in AUD$

Employment Income from Australia

Employment Income from United States

Employment Income from United Kingdom

Rental income from property in the United Kingdom

Dividend Income from United Kingdom (assumed as grossed up)

Interest Income from the United Kingdom

Total Gross Income

Less: Expenses :

Medical Expenses

Expenses incurred in deriving employment income from Australia

Expenses incurred in deriving employment income from the US

Expenses incurred in deriving employment income from the UK

Gift to a deductible gift recipient

Interest on debt for deriving dividend income

44,000

12,000

8,000

2,000

1,200

800

68,000

5,000

4,000

900

500

400

140

7

of Big Bank Ltd, it is surely eligible to claim input tax credit on the invoice issued by the

advertising consultants (Hopewell, 2012).

Answer to 3

Whenever an individual attains income from a country wherein he is a usual resident and from

countries as well, then he has a right to go for the foreign offset of tax. Moreover, if such

individual has income from more than one country and he has incurred expenses for attaining

such income, he can offset such expenses only if the following conditions are satisfied:

a. Such individual has paid the foreign income tax from income generated from such

foreign country, which means that tax on such income has already been paid.

b. Such person has incorporated the foreign income in the net assessable income for

computing the total tax payable on income (Hopewell, 2012).

Computation of Assessable Income and Foreign Tax Offset:

Particulars Amount in AUD$

Employment Income from Australia

Employment Income from United States

Employment Income from United Kingdom

Rental income from property in the United Kingdom

Dividend Income from United Kingdom (assumed as grossed up)

Interest Income from the United Kingdom

Total Gross Income

Less: Expenses :

Medical Expenses

Expenses incurred in deriving employment income from Australia

Expenses incurred in deriving employment income from the US

Expenses incurred in deriving employment income from the UK

Gift to a deductible gift recipient

Interest on debt for deriving dividend income

44,000

12,000

8,000

2,000

1,200

800

68,000

5,000

4,000

900

500

400

140

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

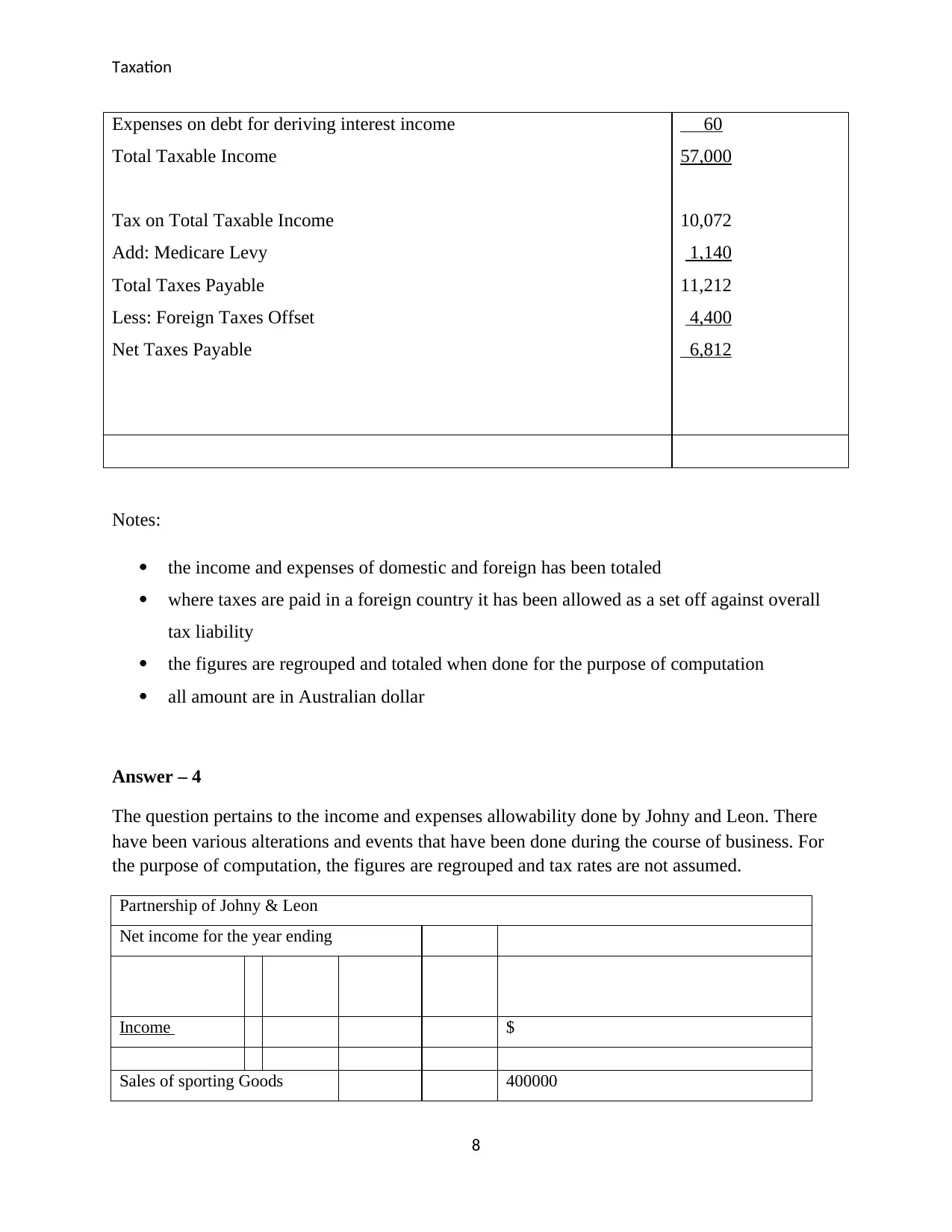

Expenses on debt for deriving interest income

Total Taxable Income

Tax on Total Taxable Income

Add: Medicare Levy

Total Taxes Payable

Less: Foreign Taxes Offset

Net Taxes Payable

60

57,000

10,072

1,140

11,212

4,400

6,812

Notes:

the income and expenses of domestic and foreign has been totaled

where taxes are paid in a foreign country it has been allowed as a set off against overall

tax liability

the figures are regrouped and totaled when done for the purpose of computation

all amount are in Australian dollar

Answer – 4

The question pertains to the income and expenses allowability done by Johny and Leon. There

have been various alterations and events that have been done during the course of business. For

the purpose of computation, the figures are regrouped and tax rates are not assumed.

Partnership of Johny & Leon

Net income for the year ending

Income $

Sales of sporting Goods 400000

8

Expenses on debt for deriving interest income

Total Taxable Income

Tax on Total Taxable Income

Add: Medicare Levy

Total Taxes Payable

Less: Foreign Taxes Offset

Net Taxes Payable

60

57,000

10,072

1,140

11,212

4,400

6,812

Notes:

the income and expenses of domestic and foreign has been totaled

where taxes are paid in a foreign country it has been allowed as a set off against overall

tax liability

the figures are regrouped and totaled when done for the purpose of computation

all amount are in Australian dollar

Answer – 4

The question pertains to the income and expenses allowability done by Johny and Leon. There

have been various alterations and events that have been done during the course of business. For

the purpose of computation, the figures are regrouped and tax rates are not assumed.

Partnership of Johny & Leon

Net income for the year ending

Income $

Sales of sporting Goods 400000

8

Taxation

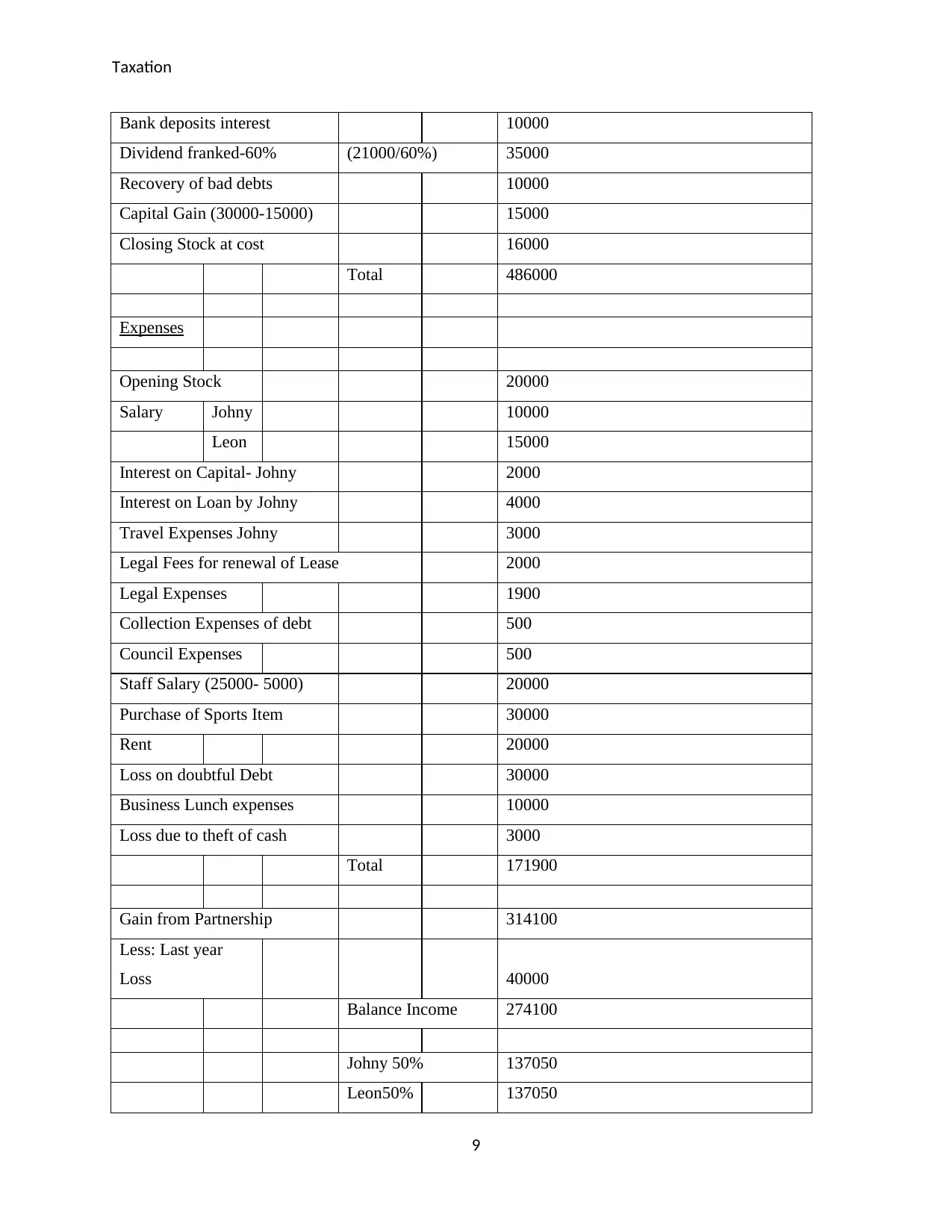

Bank deposits interest 10000

Dividend franked-60% (21000/60%) 35000

Recovery of bad debts 10000

Capital Gain (30000-15000) 15000

Closing Stock at cost 16000

Total 486000

Expenses

Opening Stock 20000

Salary Johny 10000

Leon 15000

Interest on Capital- Johny 2000

Interest on Loan by Johny 4000

Travel Expenses Johny 3000

Legal Fees for renewal of Lease 2000

Legal Expenses 1900

Collection Expenses of debt 500

Council Expenses 500

Staff Salary (25000- 5000) 20000

Purchase of Sports Item 30000

Rent 20000

Loss on doubtful Debt 30000

Business Lunch expenses 10000

Loss due to theft of cash 3000

Total 171900

Gain from Partnership 314100

Less: Last year

Loss 40000

Balance Income 274100

Johny 50% 137050

Leon50% 137050

9

Bank deposits interest 10000

Dividend franked-60% (21000/60%) 35000

Recovery of bad debts 10000

Capital Gain (30000-15000) 15000

Closing Stock at cost 16000

Total 486000

Expenses

Opening Stock 20000

Salary Johny 10000

Leon 15000

Interest on Capital- Johny 2000

Interest on Loan by Johny 4000

Travel Expenses Johny 3000

Legal Fees for renewal of Lease 2000

Legal Expenses 1900

Collection Expenses of debt 500

Council Expenses 500

Staff Salary (25000- 5000) 20000

Purchase of Sports Item 30000

Rent 20000

Loss on doubtful Debt 30000

Business Lunch expenses 10000

Loss due to theft of cash 3000

Total 171900

Gain from Partnership 314100

Less: Last year

Loss 40000

Balance Income 274100

Johny 50% 137050

Leon50% 137050

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

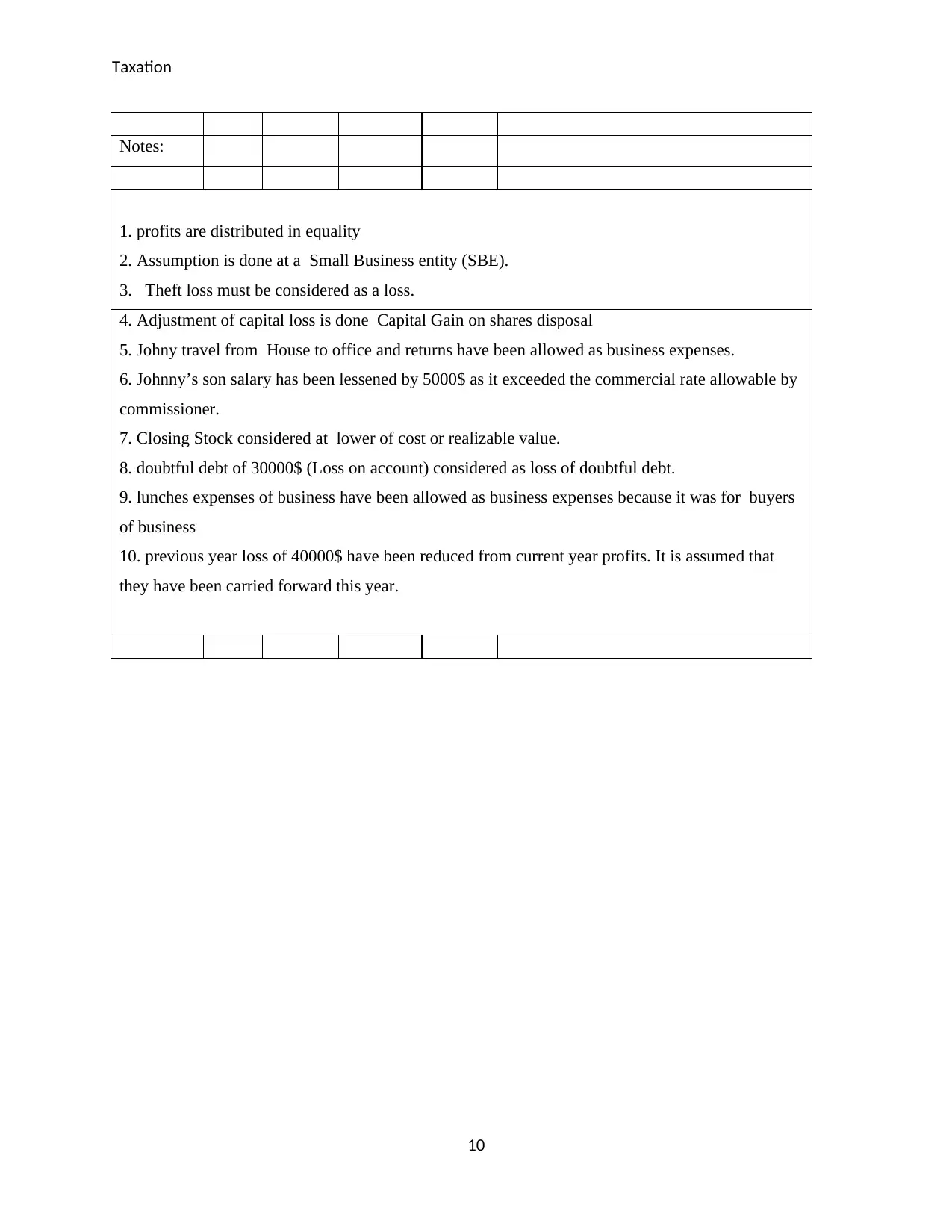

Notes:

1. profits are distributed in equality

2. Assumption is done at a Small Business entity (SBE).

3. Theft loss must be considered as a loss.

4. Adjustment of capital loss is done Capital Gain on shares disposal

5. Johny travel from House to office and returns have been allowed as business expenses.

6. Johnny’s son salary has been lessened by 5000$ as it exceeded the commercial rate allowable by

commissioner.

7. Closing Stock considered at lower of cost or realizable value.

8. doubtful debt of 30000$ (Loss on account) considered as loss of doubtful debt.

9. lunches expenses of business have been allowed as business expenses because it was for buyers

of business

10. previous year loss of 40000$ have been reduced from current year profits. It is assumed that

they have been carried forward this year.

10

Notes:

1. profits are distributed in equality

2. Assumption is done at a Small Business entity (SBE).

3. Theft loss must be considered as a loss.

4. Adjustment of capital loss is done Capital Gain on shares disposal

5. Johny travel from House to office and returns have been allowed as business expenses.

6. Johnny’s son salary has been lessened by 5000$ as it exceeded the commercial rate allowable by

commissioner.

7. Closing Stock considered at lower of cost or realizable value.

8. doubtful debt of 30000$ (Loss on account) considered as loss of doubtful debt.

9. lunches expenses of business have been allowed as business expenses because it was for buyers

of business

10. previous year loss of 40000$ have been reduced from current year profits. It is assumed that

they have been carried forward this year.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

References

Martin, D 2001 Input Tax Credits - The Core Mechanism of GST, viewed 11 September 2017

http://www.tved.net.au/index.cfm?SimpleDisplay=PaperDisplay.cfm&PaperDisplay=http://

www.tved.net.au/PublicPapers/

June_2001,_Sound_Education_in_GST,_Input_Tax_Credits___The_Core_Mechanism_of_GST.

html

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 12 September 2017,

www.zdnet.com.au.

Fullerton,I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax

Handbook Tax Return Edition 2017, Thomson Reuters

Kenny, P, Blissenden, M, & Villios, S 2016, Australian Tax 2017, Thomson Reuters: Australia

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation

Press

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Renton N.E 2005, Income Tax and Investment, 2nd edition, Sydney

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A 2017,

Principles of Taxation Law 2017, Law book Australia

11

References

Martin, D 2001 Input Tax Credits - The Core Mechanism of GST, viewed 11 September 2017

http://www.tved.net.au/index.cfm?SimpleDisplay=PaperDisplay.cfm&PaperDisplay=http://

www.tved.net.au/PublicPapers/

June_2001,_Sound_Education_in_GST,_Input_Tax_Credits___The_Core_Mechanism_of_GST.

html

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 12 September 2017,

www.zdnet.com.au.

Fullerton,I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax

Handbook Tax Return Edition 2017, Thomson Reuters

Kenny, P, Blissenden, M, & Villios, S 2016, Australian Tax 2017, Thomson Reuters: Australia

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation

Press

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Renton N.E 2005, Income Tax and Investment, 2nd edition, Sydney

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A 2017,

Principles of Taxation Law 2017, Law book Australia

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.