Financial Analysis Report: Sainsbury and Tesco for Market Share

VerifiedAdded on 2021/02/20

|32

|5554

|53

Report

AI Summary

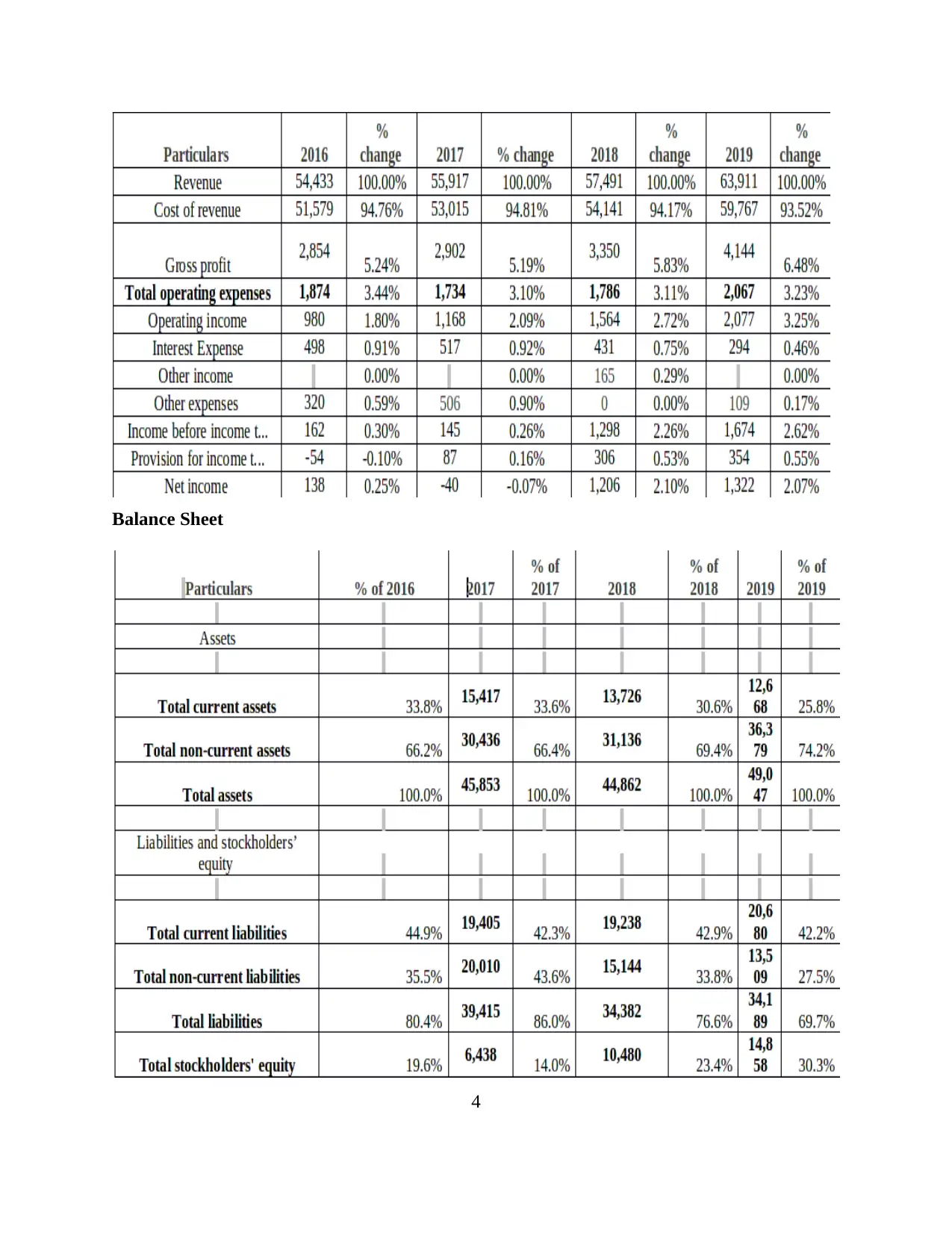

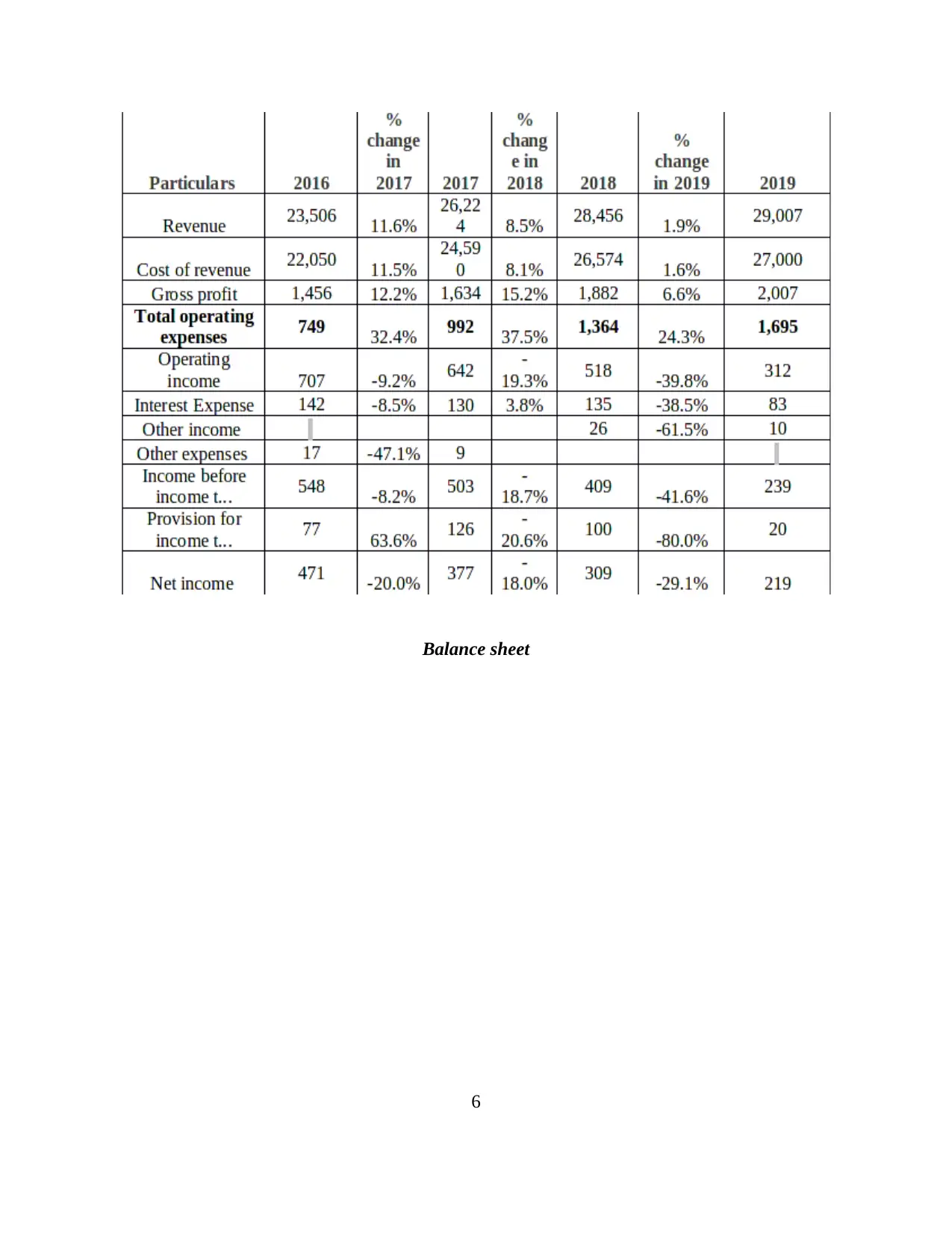

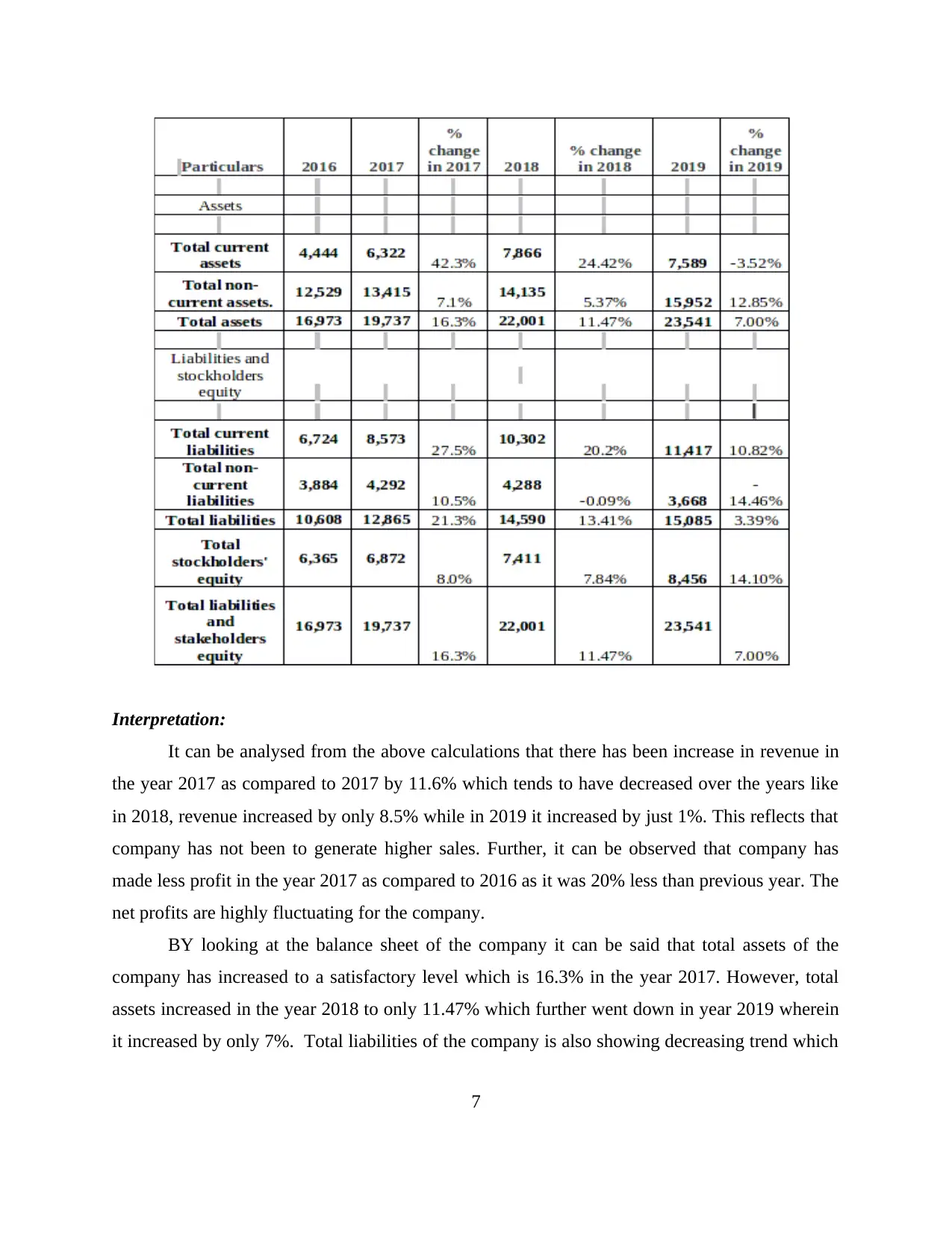

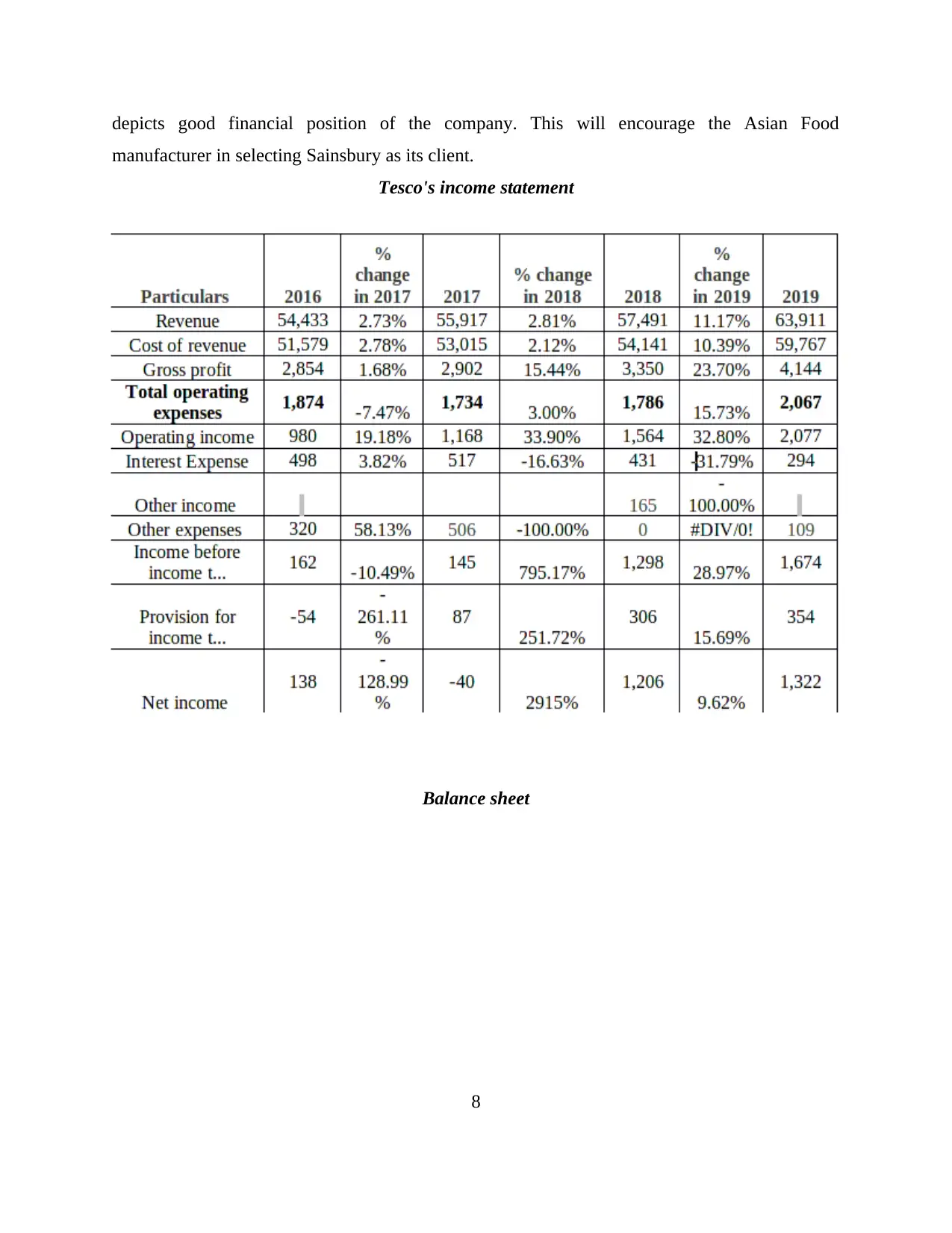

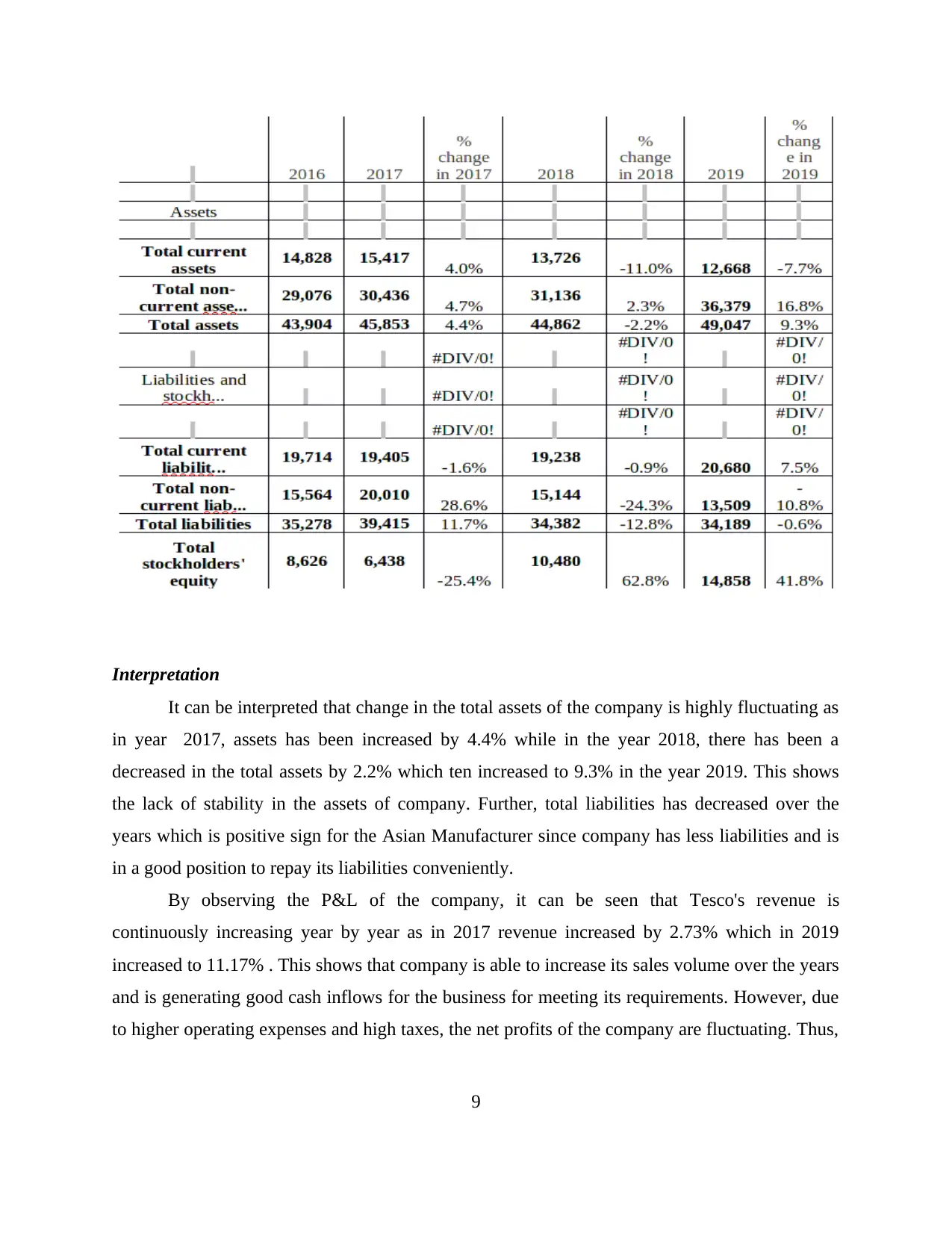

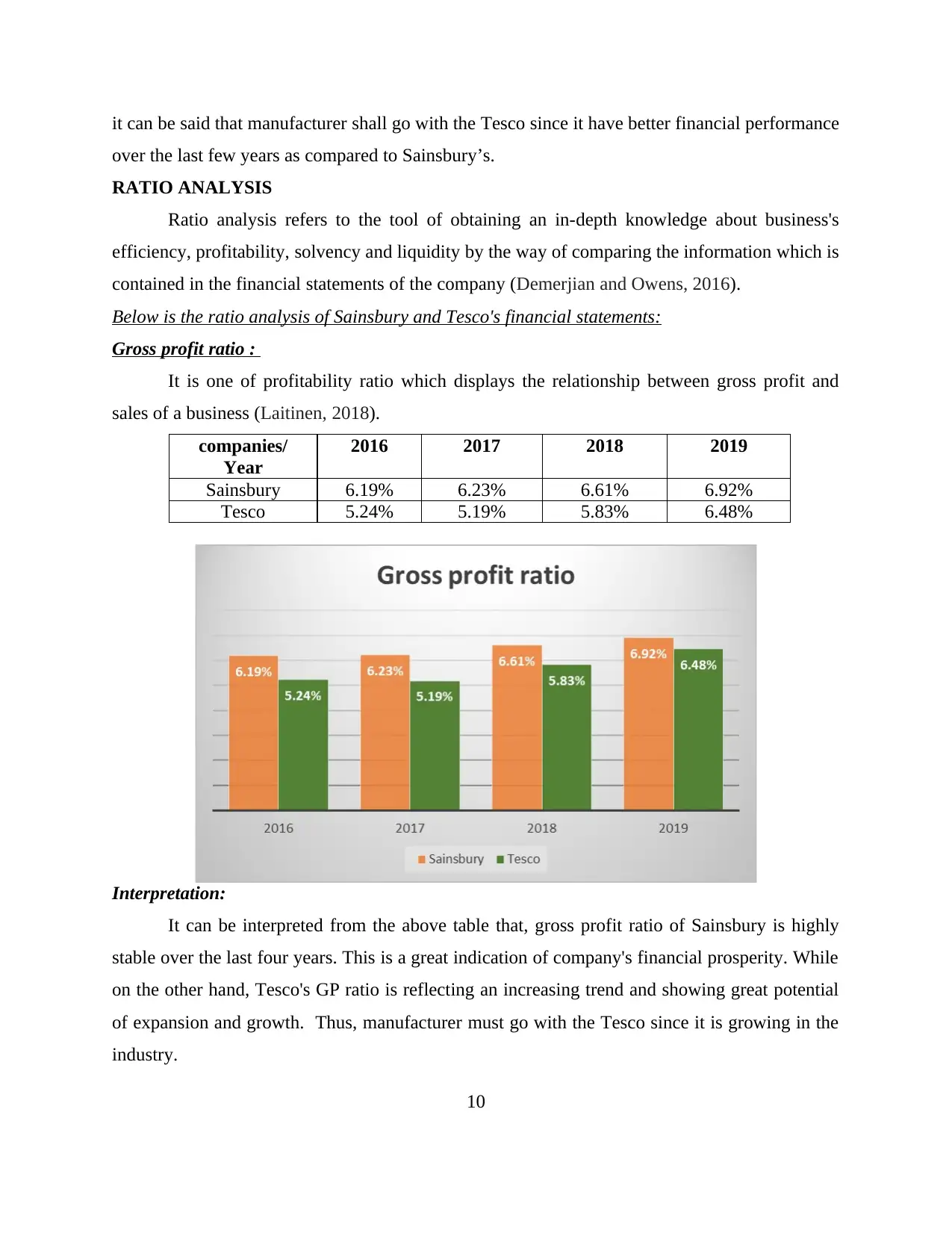

This report offers a comprehensive financial analysis of two major UK supermarket chains, Sainsbury and Tesco, aiming to assess their financial health and identify potential business opportunities. The analysis employs vertical, horizontal, and ratio analysis techniques to evaluate their income statements and balance sheets over several years. It delves into the importance of working capital analysis for informed decision-making and critically examines their cash flow statements. The report includes detailed calculations for ratio analysis, along with interpretations of key financial metrics like gross profit ratio, net profit ratio, current ratio, quick ratio, debt-equity ratio, and inventory turnover ratio. The findings are presented to assist an Asian food manufacturer in selecting the most suitable supermarket chain to expand its market share. The report emphasizes the financial performance, profitability, liquidity, and solvency of both companies to guide the manufacturer's strategic decision-making process. The report concludes by providing recommendations to the manufacturer based on the financial analysis of the two supermarkets.

1 out of 32

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.