Which Stock Should I Invest In PHUONG THAO BUI

VerifiedAdded on 2023/05/05

|11

|2540

|64

AI Summary

In this report we will discuss about Investing and below are the summaries point:-

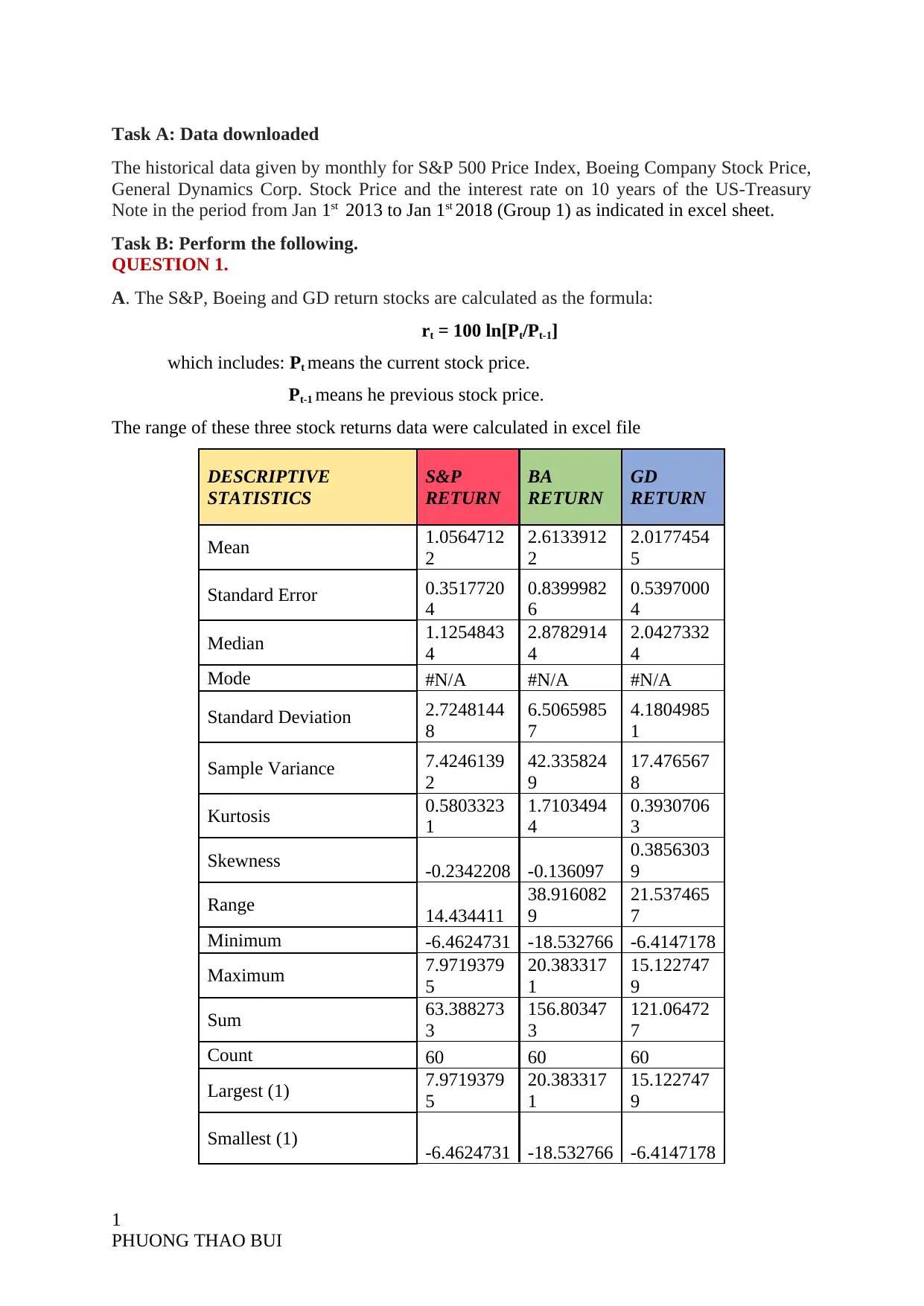

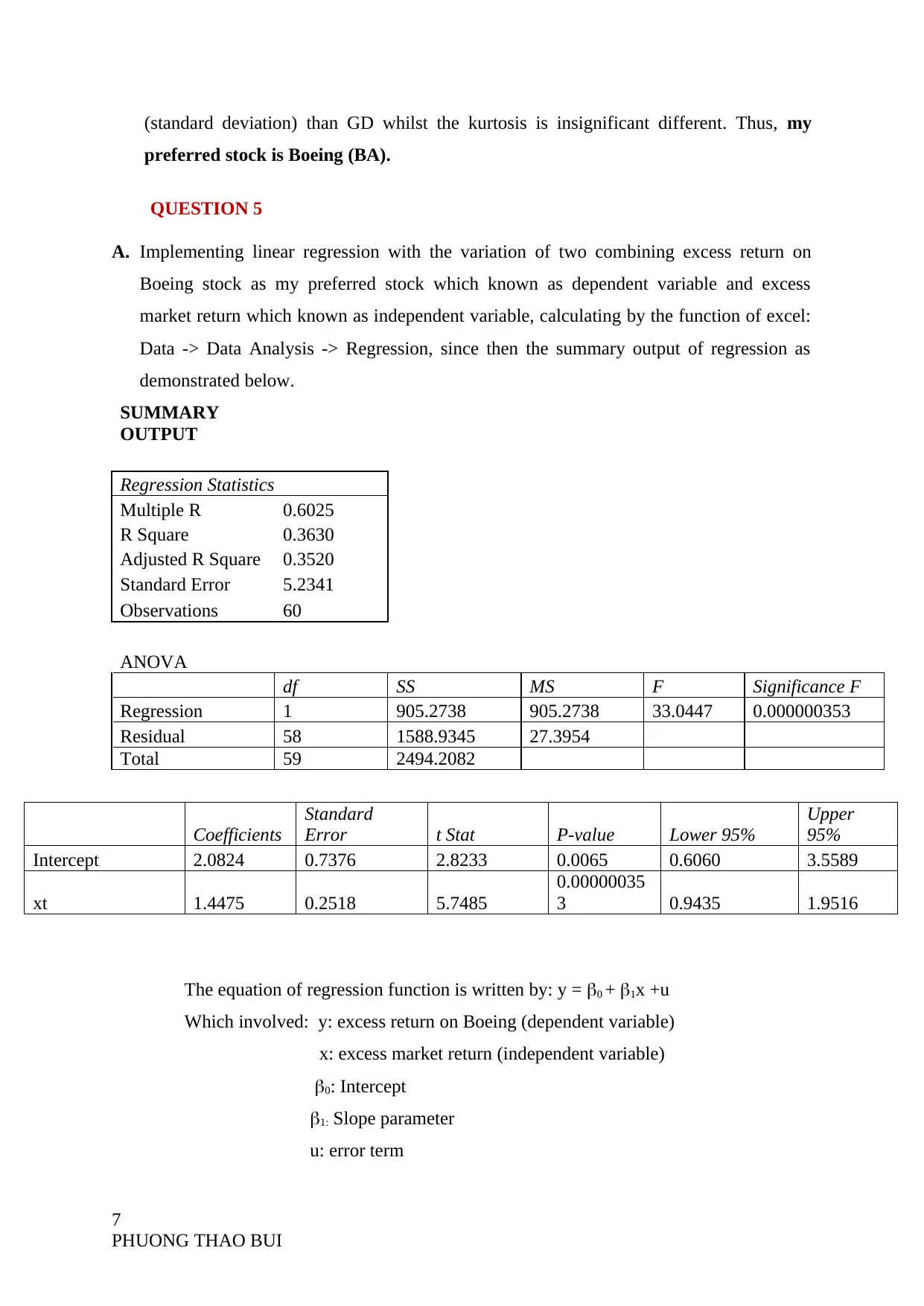

Monthly historical data was given for S&P 500 Price Index, Boeing Company Stock Price, General Dynamics Corp. Stock Price, and interest rate on 10 years of the US-Treasury Note from Jan 1st 2013 to Jan 1st 2018 (Group 1).

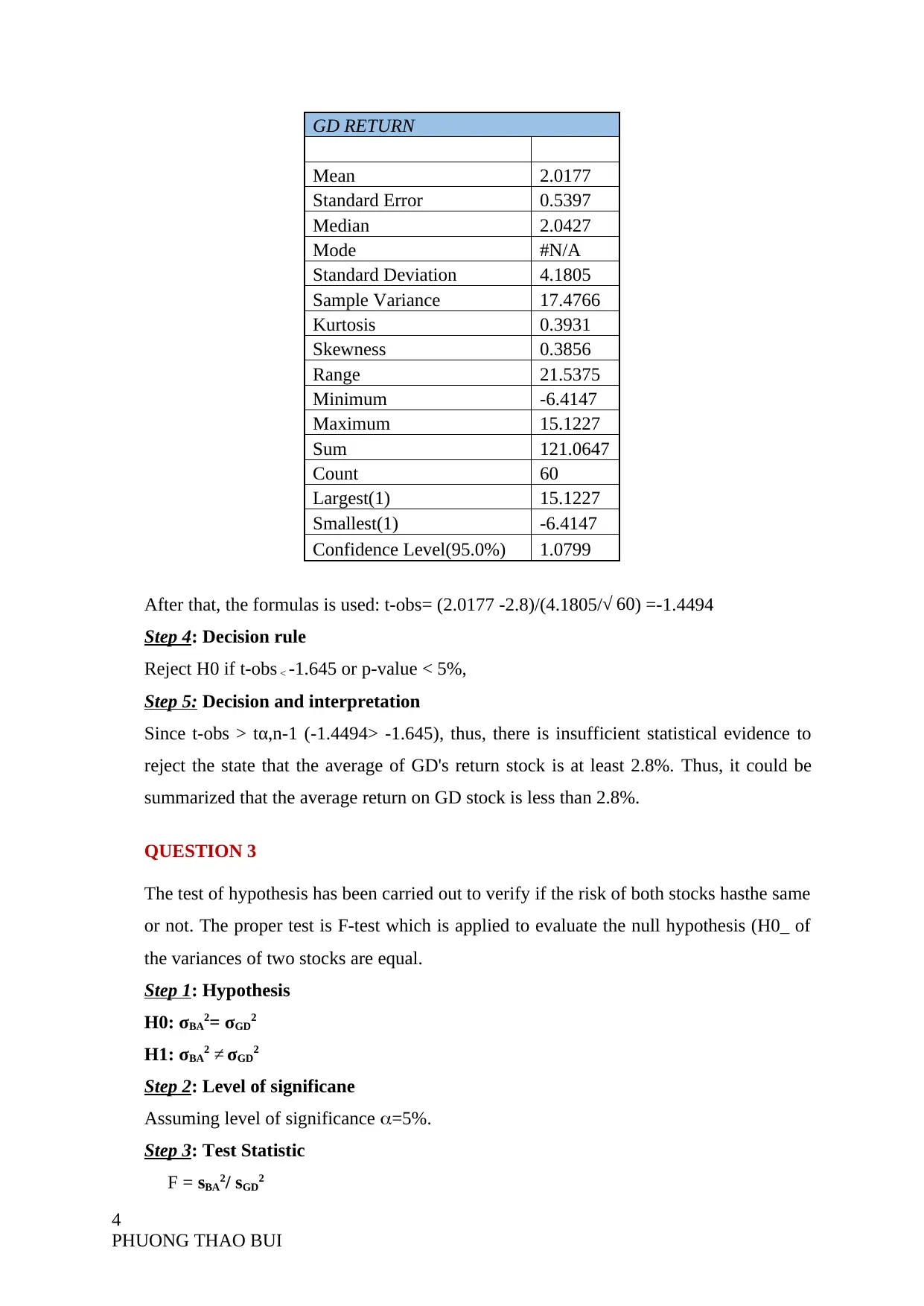

The average return and standard deviation of Boeing (BA) stocks were 2.6134 and 6.5066 respectively, while GD stocks had an average return of 2.0177 with a standard deviation of 4.1805.

Boeing Company had a higher average return than that of General Dynamics Corporate, but BA stock was riskier than GD stocks based on the standard deviation.

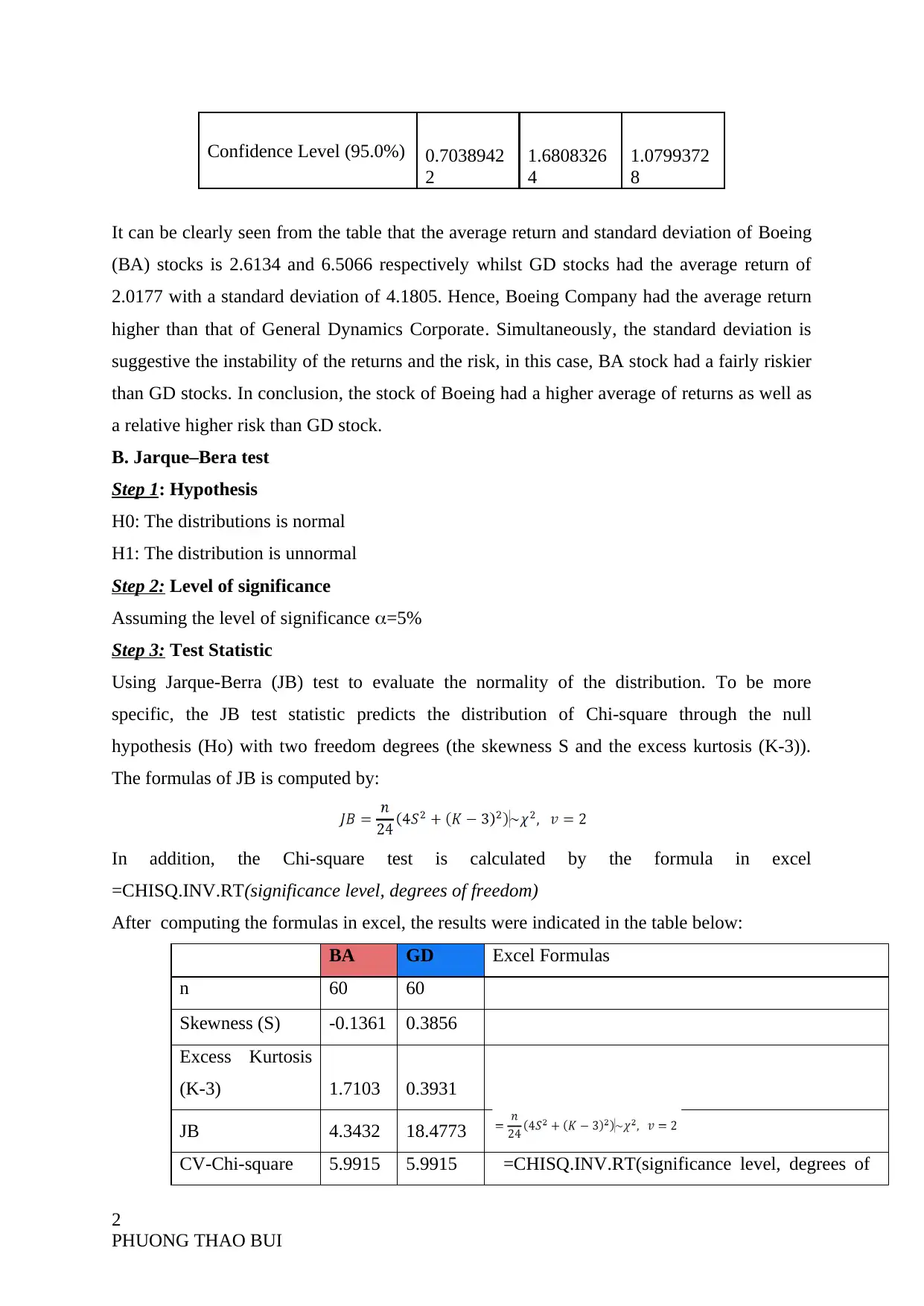

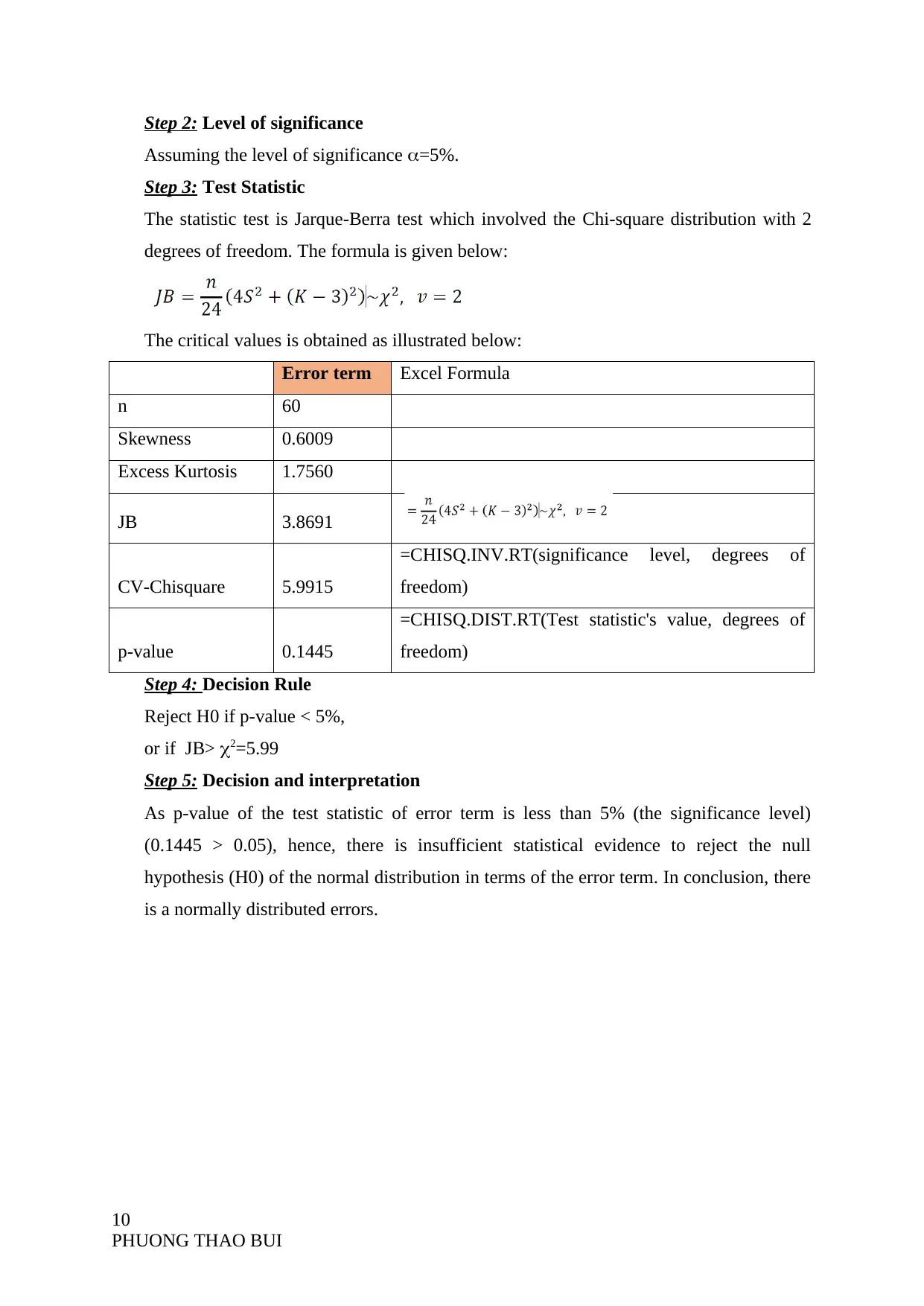

The null hypothesis (H0) was that the distribution of both stocks was normal, and the alternative hypothesis (H1) was that the distribution was unnormal with a level of significance of 5%.

The Jarque-Berra (JB) test was used to evaluate the normality of the distribution, and the test statistic was computed using the formulas for JB.

For BA return stock, the null hypothesis was not rejected as p-value > 5% and the JB value < CV-Chisquare.

For GD return stock, the null hypothesis was rejected as p-value < 5% and the JB value > CV-Chisquare.

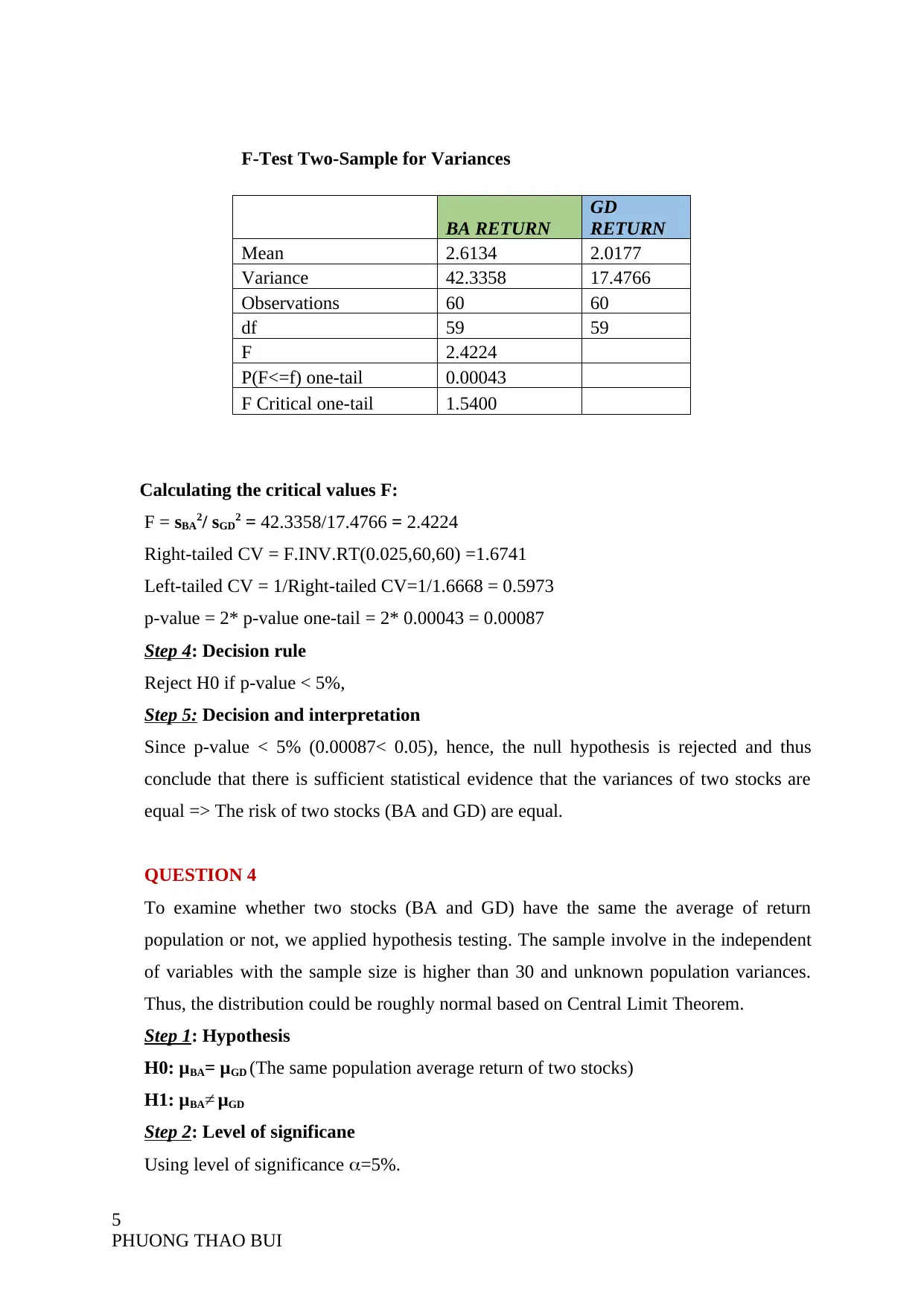

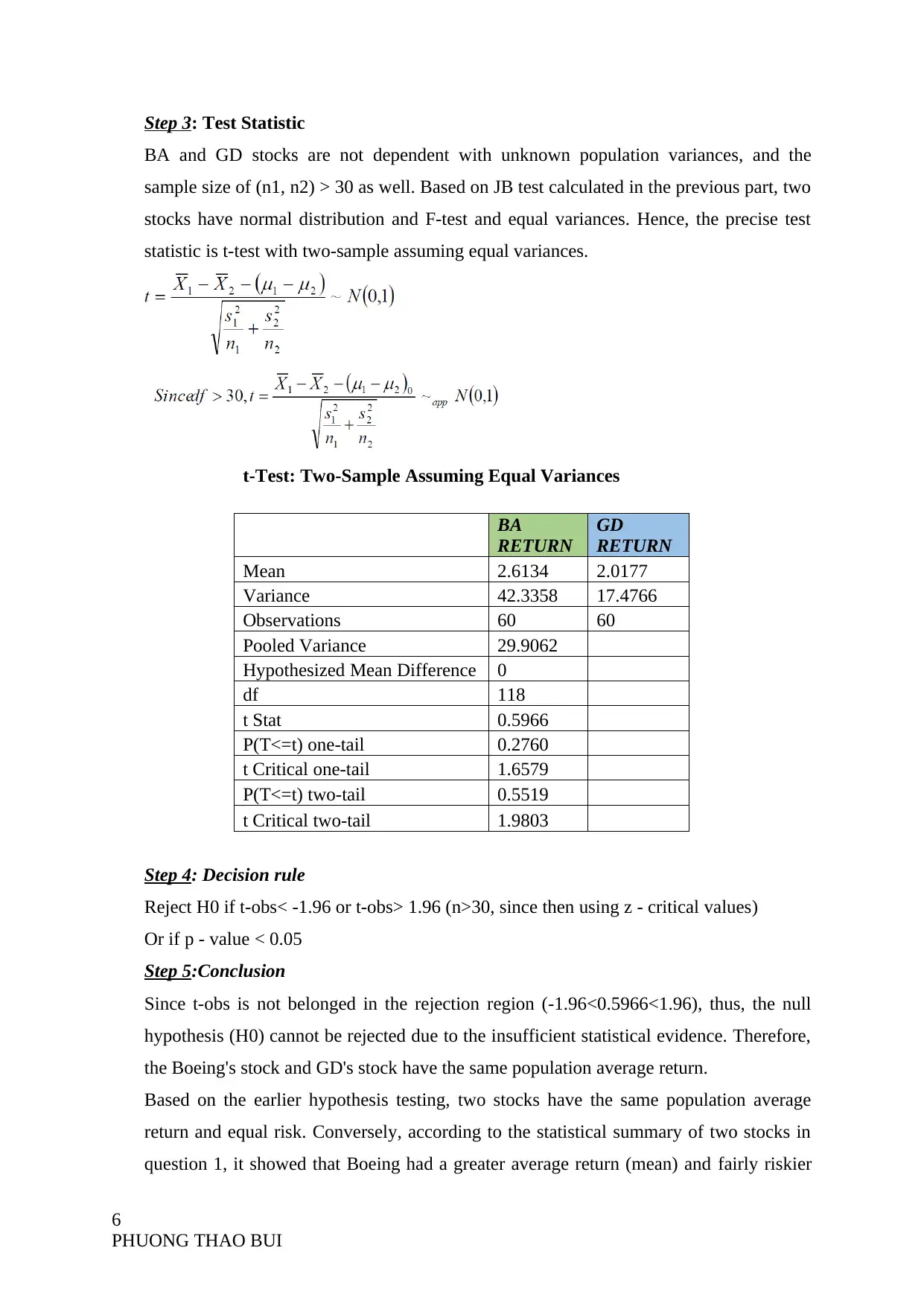

The F-test was used to test the null hypothesis that the variances of the two stocks were equal.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.